Everything Says Buy. Almost Everything.

Market Recap — June 21th 2026

2026-06-21 · 10 min read · Originally published on Substack ↗

TL;DR

A wide bounce the heavy money has not signed off on. Participation is broad and new highs dominate, but the short-term thrust has stalled and volume keeps leaning to the sellers. The kind of tape that snaps into motion the moment conviction shows up, one way or the other.

The market is making a concentrated, rate-sensitive bet. The bid keeps crowding into cyclicals and abandoning everything else instead of broadening, which is the opposite of what a recovery does off a base. The groups carrying it are also the ones most exposed if the bond picture turns.

The vol complex is calm, with one nervous corner. Broad volatility, the curve, and vol-of-vol all read normal. The single exception is tech vol, sitting near the top of its range, the same megacap concentration every other screen keeps flagging.

Hello my friends,

Four-day week. By Thursday’s close the S&P sat 2% above its 50-day, the Nasdaq ran better than 2% on the day, small caps came along, and every index I follow was stacked above its short, medium, and long trend lines at once. The trend model has not read this clean in months. On price alone, you press it.

Cast your mind back one week. We had just taken four ugly sessions in a row, your whole feed was calling the top, and I told you it looked like a flush, forced selling of the kind that says nothing about the companies being sold. Then came the one date I had circled in red, the Bank of Japan. That was the whole risk last week, the chance a hawkish Tokyo snapped the yen higher and unwound the carry trade into a global selloff. It came and went without the shock. The yen stayed soft, the carry trade held, and the worst case I had given real odds to never arrived. We bounced, and we kept it.

So the table looks clean this week, maybe too clean. The warning lives in the plumbing, not the price chart. The vol complex reads calm everywhere except the one place that matters, the fear bunched into megacap tech, the market’s own leadership, on a late-cycle backdrop of high real yields, sticky inflation, and a bond market so calm it ignores a nervous consumer. None of that breaks a clean uptrend by itself. You stay long anyway, with one hand on the door.

Last week the danger was a single circled date. This week there is none, which is the catch. The risk now is quieter and more structural: a narrow, calm tape walking into a tired cycle, with the cheapest insurance I have seen in a while.

To get the most out of these market recaps and understand the framework behind my observations, I encourage you to read about my methodology here.

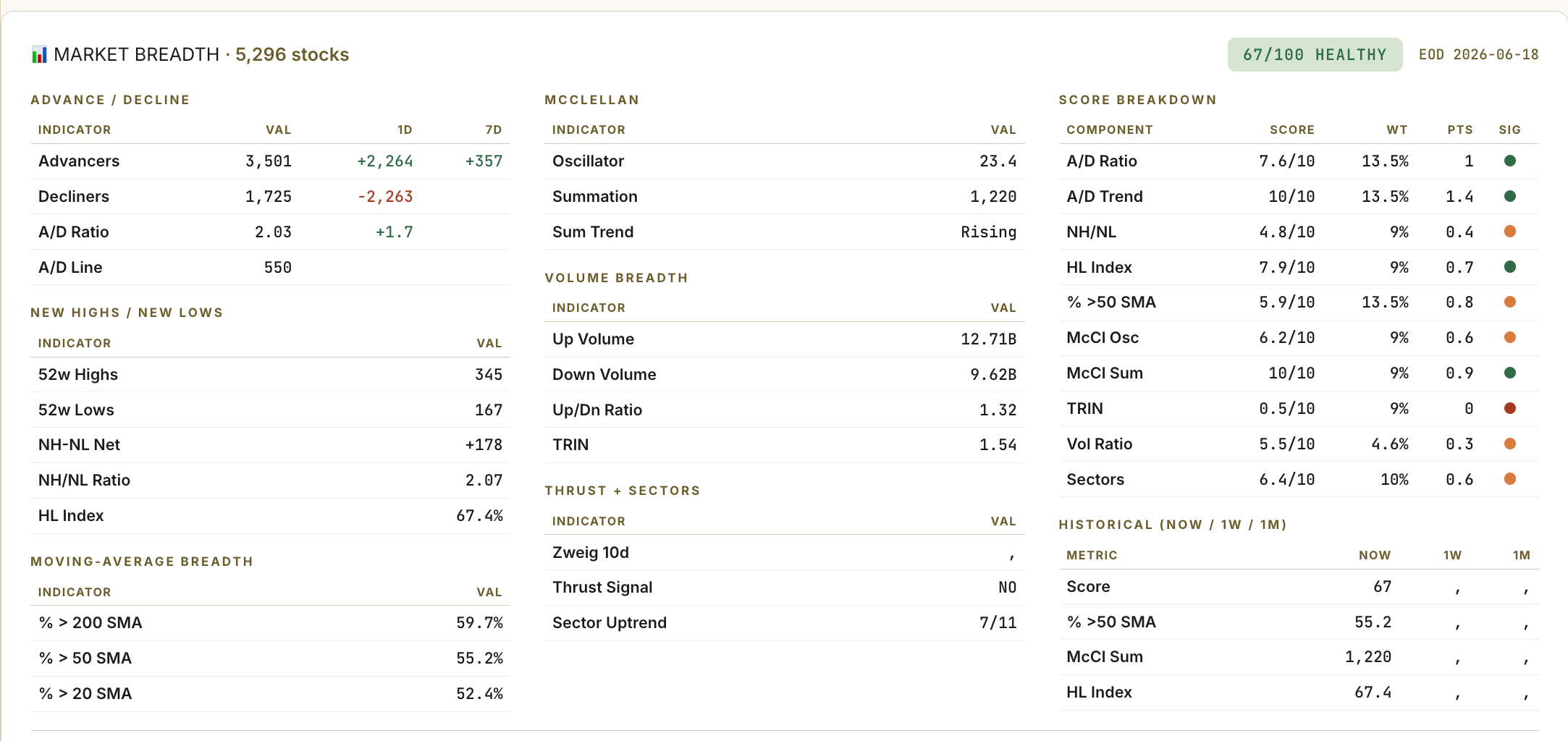

📊 Market Health

A genuine recovery the big money has not yet validated with size.

The participation is the part you can trust. New highs are burying new lows across thousands of names, the one breadth read a handful of mega-caps cannot fake, and the McClellan summation is still climbing out of the flush. Broad new highs plus a rising summation coming off forced selling is how durable rallies tend to start. The flush did no lasting structural damage.

The volume is the part that keeps me honest. The heavier dollars are still trading on the down side even as more names rise, and the short-term thrust has gone flat while price prints new highs. That last point is the quiet one. Price is making highs the deeper-timeframe breadth has not confirmed, a small negative divergence under a strong surface, the kind that evaporates if buyers commit and becomes the first crack if they walk.

So this is a recovery I hold without pressing. Institutions are letting the bounce happen without chasing it, which tells me they see the same unconfirmed tape I do. I size up when the short-term thrust catches the medium-term strength and the heavy volume turns. Until then, long but measured.

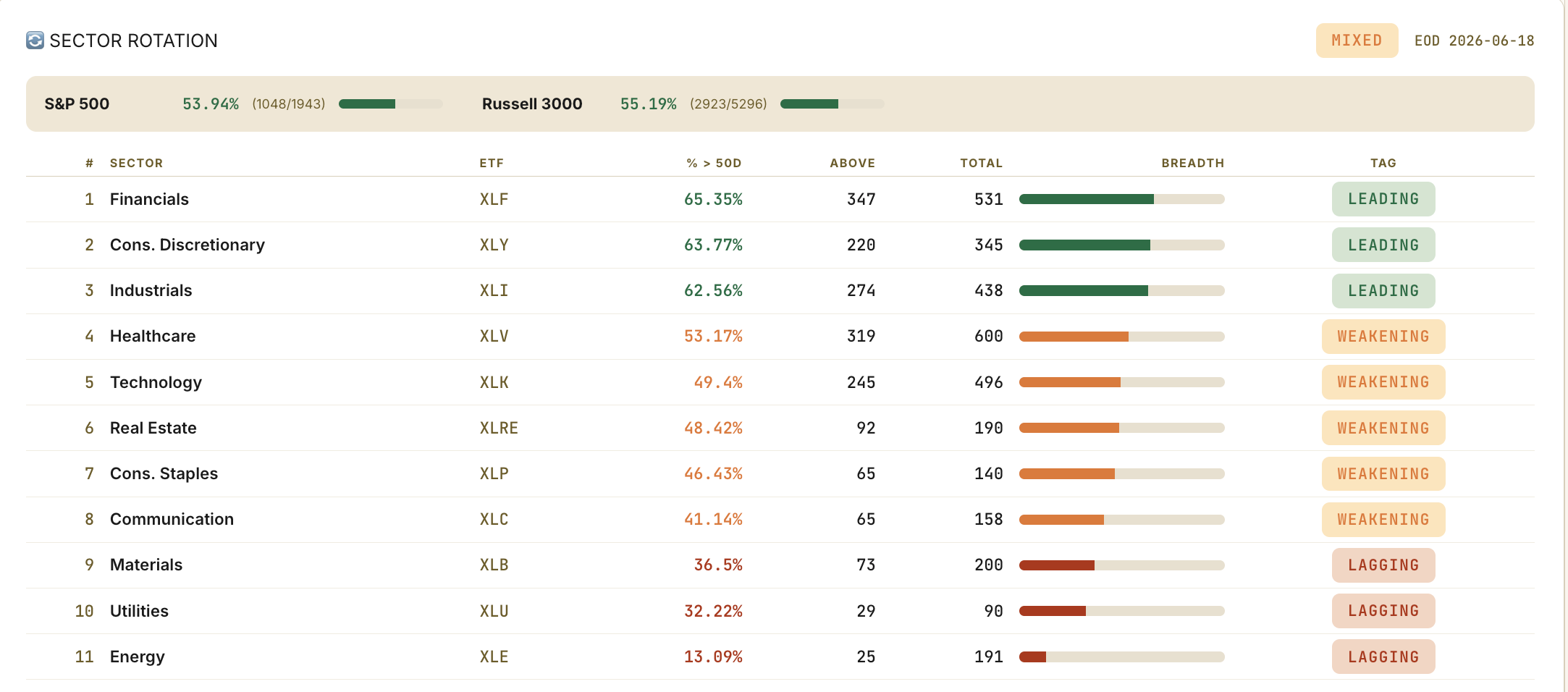

🚨 Sector Rotation

The market is buying the cycle and leaving everything else behind.

The leadership is the reflation triangle, financials and discretionary and industrials out front together. A coherent, confident bet, growth holds and rates behave, the profile you want in an expansion. The trouble is what sits under it. Off a base, a healthy recovery broadens, more groups joining as confidence returns. This one narrowed instead, the bid choosing favorites while the defensives and the commodities drained to fund them.

Technology is the sharpest tell. It tops the board on raw momentum while fewer than half its own members hold their trend, so the index’s largest weight is being carried by a thin bench of names. That is how leadership looks just before it widens or breaks.

Here is the part that ties back to the curve. The two groups doing the most work, financials and real estate, are the most rate-sensitive on the whole board. The market has poured its bet into precisely the names a late-cycle bond move would punish first. Strong leadership and fragile leadership can be the same names, and this week they are.

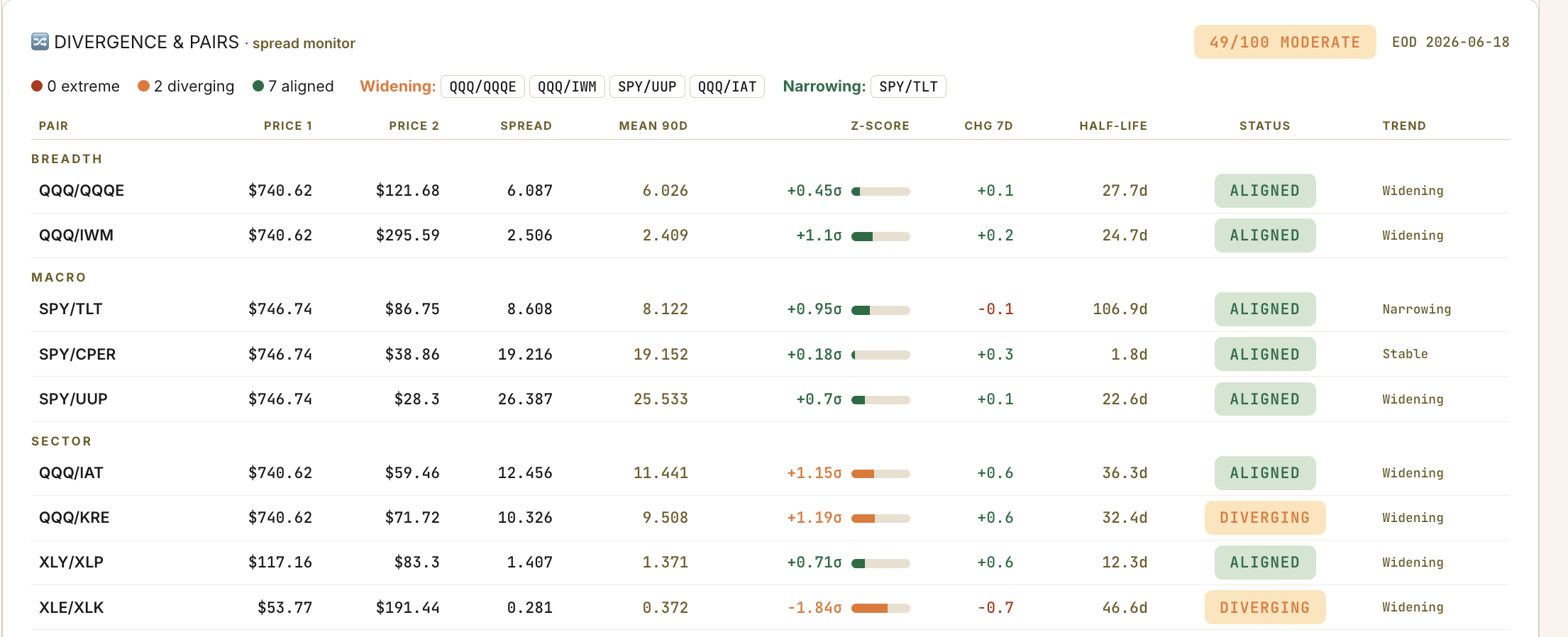

🔍 Pairs Alignment

The same concentration story, now showing up in the spreads.

Most of the board is calm. Stocks and bonds are drifting back together, the dollar sits in range, and the correlation between stocks has collapsed, which turns this into a stock-picker’s tape where selection pays and the index hides the dispersion underneath.

The one relationship that matters keeps repeating. Large-cap tech is pulling away from small caps and from the regional banks at the same time, the cleanest expression there is of money concentrating into the few names it still trusts. That is the late-cycle reflex, and it lines up with the sector narrowing and the thin tech bench from the screen above. When the same message arrives from breadth, from sectors, and now from the spreads, it stops being noise.

The chronic divergence, energy against tech, is still the widest on the board and still pulling apart. Old news, but it keeps the commodity weakness honest and reminds you the rotation here is disinflationary, a bet on rates and growth with commodities left out of the trade.

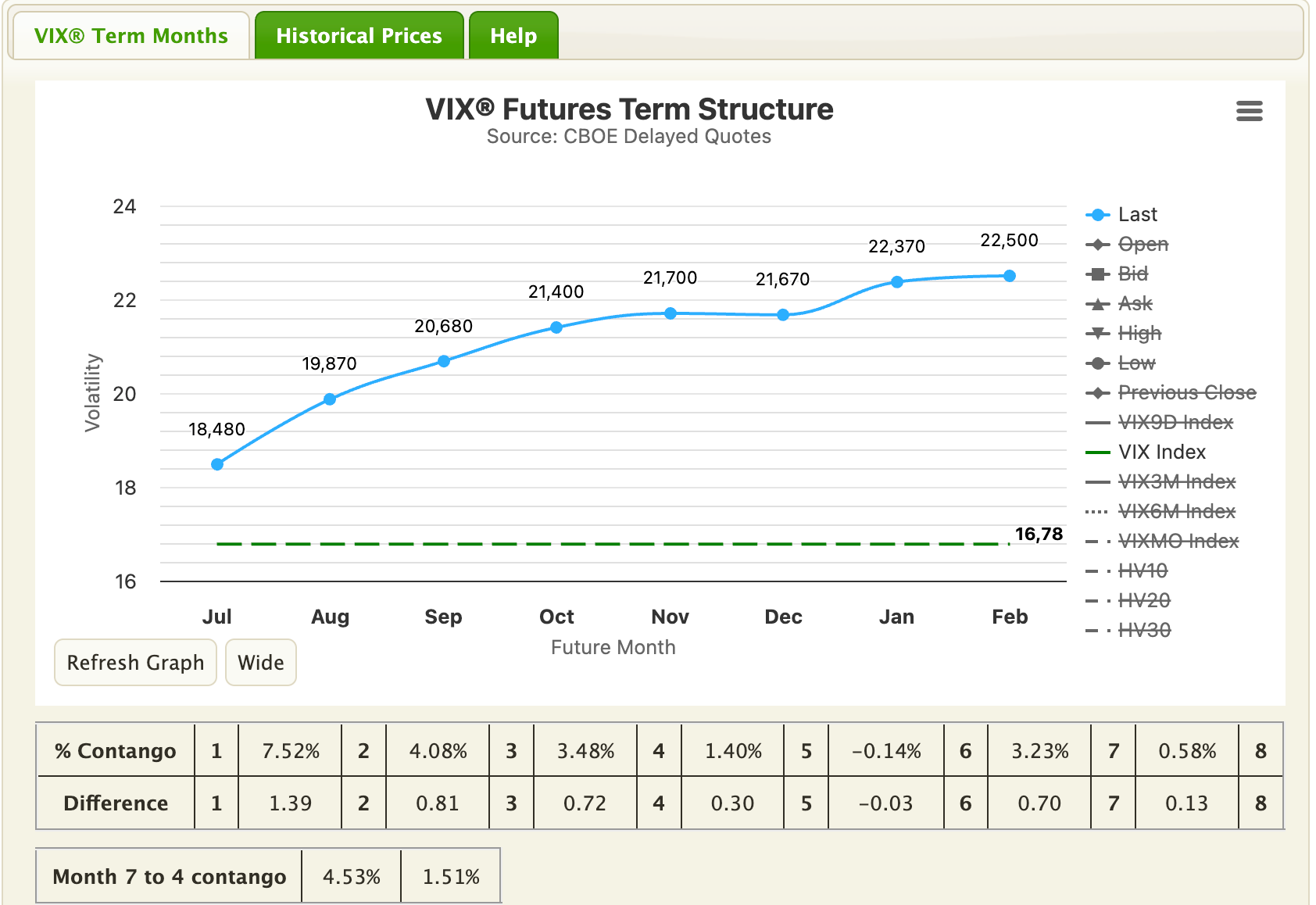

📉 Volatility

Calm across the board, with the fear bunched into the one group that leads.

The curve sits in its usual upward contango, the resting state of a calm market, not a warning. Vol-of-vol is at the floor of its range, the market’s way of saying it sees no spike coming.

The one reading that breaks ranks is the one that counts. Tech vol is the only gauge on the board flagged elevated, still near the top of its range even after cooling this week, and rich against the broad market. The options market is relaxed about stocks in general and wary of megacap tech in particular, the same group breadth, sectors and pairs have flagged all week. Four screens now point at one place. The fear is concentrated in one corner, and that corner is the market’s own leadership.

So the signal is narrow. You do not hedge the index off this screen, it says quiet and cheap. If you hedge anything, you hedge the tech concentration, the single spot showing strain everywhere you look.

💱 FX

Currencies are still voting risk-on.

The dollar is firm and the yen keeps sliding, parked near the same line around 160 that had everyone holding their breath last week. The level has not moved, the calendar has. With the Bank of Japan behind us and nothing circled this week, the carry trade the weak yen funds is dormant rather than defused. It still runs, it remains the largest single fault line in global markets, and it still has no near-term trigger. So the tape reads risk-on for now, with the spring left armed.

The franc is the one I keep a finger on, the cleanest safe-haven in the group and the first place fear shows when funding tightens. As long as it stays soft against a weak euro, currencies are endorsing the equity regime. The day the franc turns higher is the day to take the rest of this letter more seriously. Not this week.

🧠 My Take

The clean uptrend is real and the broad participation gives it a foundation, which is why I am not leaning bearish. The caution comes from three things that rhyme: the heavy volume never confirmed the bounce, the leadership narrowed into the most rate-sensitive corners and the fear in the options market is bunched into tech, the exact leadership the rally leans on. I stay long and carry real respect for that gap.

How the week breaks down:

The orderly path, base case, ~50%. The short-term thrust catches the medium-term strength, leadership finally broadens past the cyclical corners, and the market grinds higher off a base that already has wide participation behind it. Expiration is cleared and the buyers who sat out the quiet week step in. The breadth backs this one most.

The repricing, the real risk, ~30%. The tech-vol warning turns out right. A late-cycle catalyst, a hot print or a credit wobble, forces a reprice, the nervous tech vol bleeds into the broad market, and the narrow leadership cracks where it is thinnest. The rate-sensitive leaders take the first and hardest hit, exactly because they led on the way up. This is the scenario the hedge exists for.

The stall, ~20%. Nothing resolves. The volume stays absent, the breadth cannot broaden, and the tape chops below its highs until the next catalyst.

I am long, tilted toward the cyclical leaders and quality pullbacks and away from the commodity laggards. I carry a little downside insurance broad vol makes nearly free, aimed at the tech concentration, the one corner showing strain.

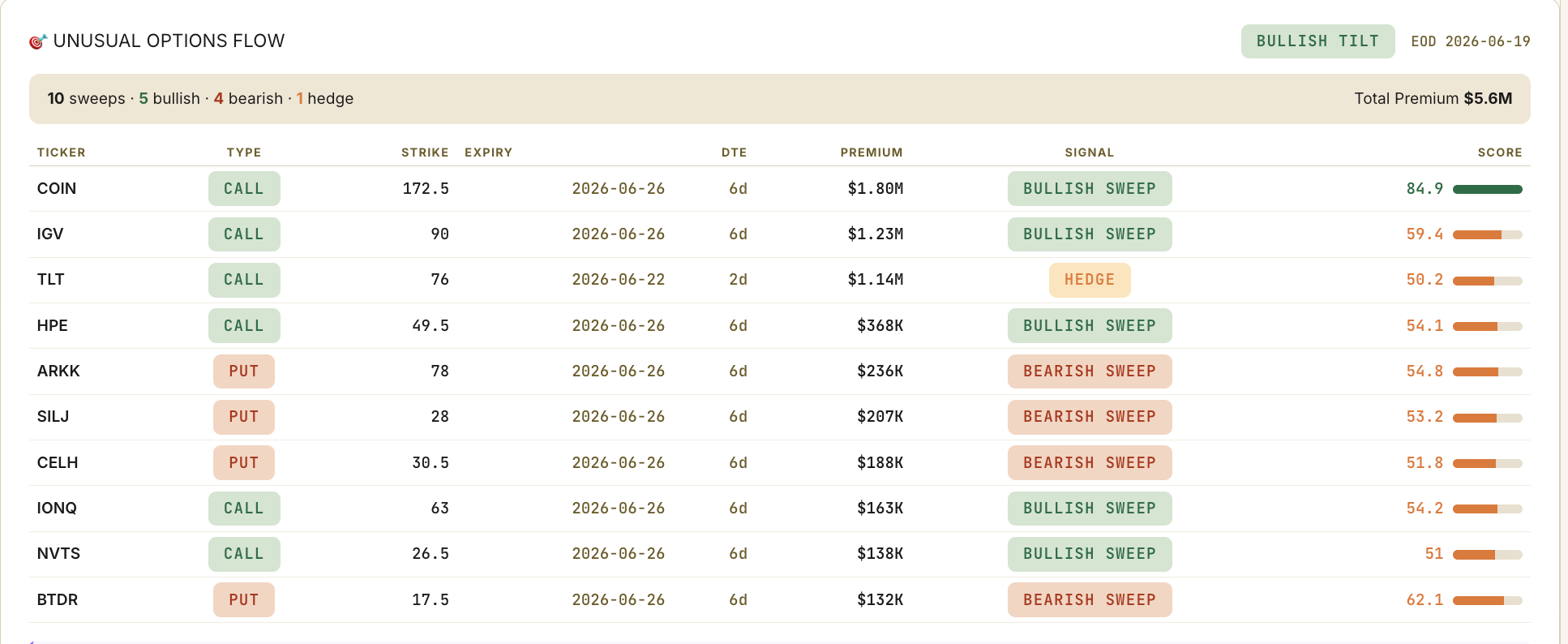

🔎 Options Flow

The largest premium of the week went into upside on a crypto-exchange name and a basket of software, and that software bid sits exactly where I want to be long. So far, so risk-on.

Underneath it, the single biggest hedge on the board was a grab for long-dated Treasuries. That is a desk quietly buying duration, positioning for a rotation into bonds even while it stays long equities. The options-market version of one hand on the door.

The downside bets cluster where this letter is already soft, the high-beta growth corner and the speculative names that run hottest when the tape is loose. When the most aggressive money aims its puts at the frothiest part of the market and pays up for bond protection at the same time, the message holds together: lean long, keep the exit in sight.

🔥 Trade of the Week:

A great business at a price nobody would pay six months ago.

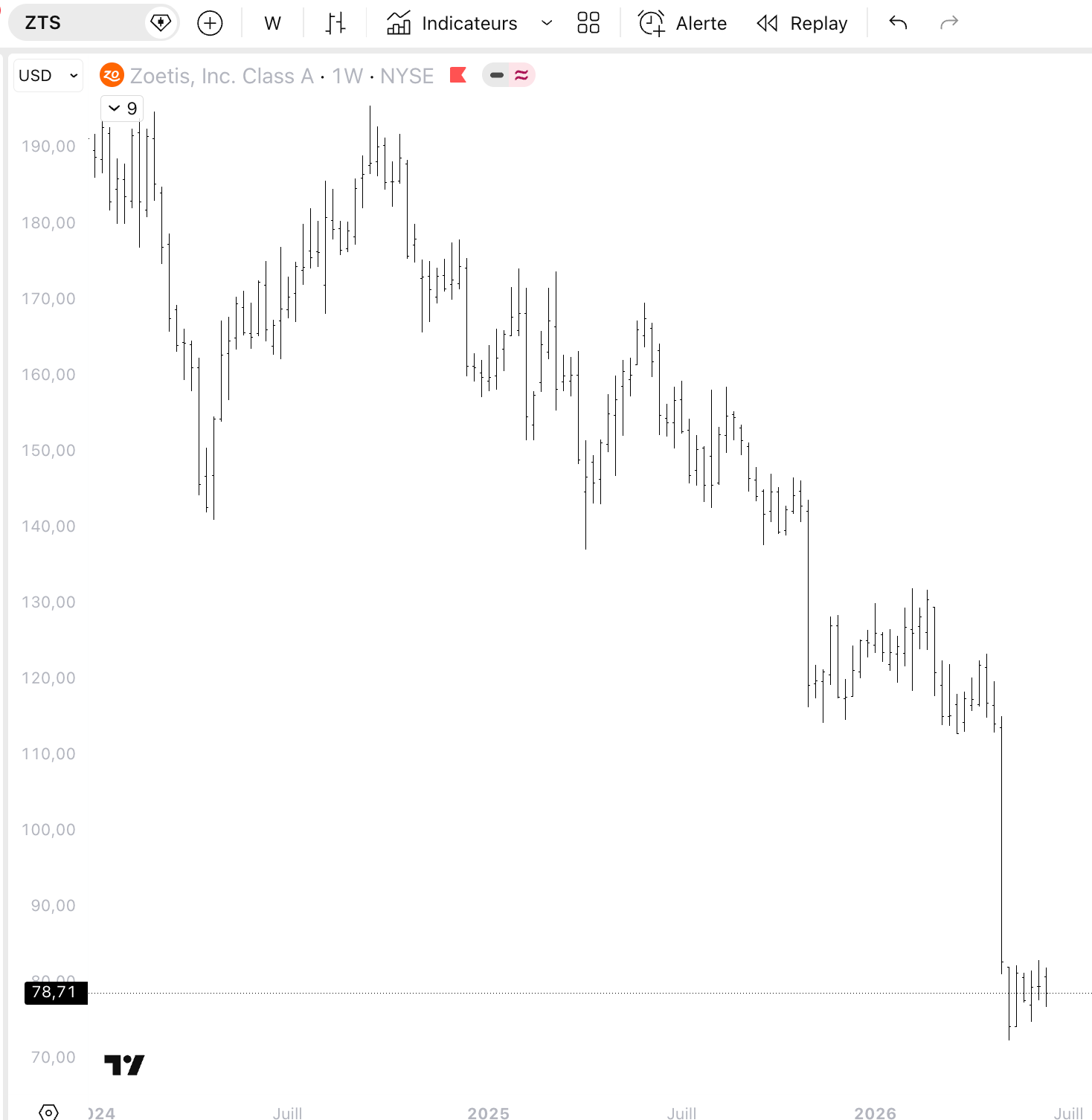

Zoetis is a falling knife, the chart is ugly, and I am putting it here anyway, as a contrarian starter, because the best risk-reward sometimes hides in the name the tape has given up on.

The case is the quality.

Zoetis is the leader in animal health with pricing power that does not evaporate in a year. And it is down roughly two thirds from its 2022 peak of $235, sitting near $78, back to levels it last saw years ago. The selling looks tired, and price is testing a floor the stock based on during the way up. Blood in the streets: you buy it while the panic is loud, before it ever feels safe.

Now the honest part. The 30-week trend is still falling, so you are early by definition, and calling a bottom in a downtrend is the hardest trade there is. No desk is recommending it and the flow gives no cover. If being wrong fast bothers you, wait for the base to build and skip this one.

Entry around $78.71, scaling in toward the prior low in pieces.

Stop $71.50, a weekly close below the multi-year low says the bottom is not in.

Target $95, the shelf it broke down from.

R:R roughly 2 to 1 here.

Size small, a starter position

What kills it is a weekly close below $71.50. That takes out the multi-year low, proves the knife is still falling, and ends the trade. Lose the level, lose the reason to be there.

See you next week,

Daniel

Disclaimer

This newsletter is for educational and informational purposes only. It is not financial advice.

The content reflects personal opinions shared publicly as a journal. Trading stocks, options, futures, or any financial instrument involves significant risk. You can lose your entire investment. There is no guarantee of profit.

The author is not a registered investment advisor, broker, or financial professional with any regulatory authority including the SEC or CFTC. Always consult a licensed financial advisor before making any investment decisions.

By reading this newsletter, you accept full responsibility for your own trading and investment choices. Past performance does not guarantee future results. Markets are unpredictable.

Screenshots are courtesy of TradingView, VixCentral, and other platforms with which the author has no affiliation. Information shared may contain errors or become outdated quickly.

This content is the intellectual property of the author. Copying or redistributing without permission is prohibited.

By continuing to read, you acknowledge and accept these terms.

Read the desk every week

Market analysis in plain English, plus the app that scans the whole US market for you.

Become a member Read the original on Substack ↗