The Ceasefire Died. The Rally Didn't.

Market Recap — July 11th 2026 · The Philosopher Investor

2026-07-11 · 12 min read · Originally published on Substack ↗

Hello my friends,

On Wednesday the United States struck Iran for a second night and the President declared the interim agreement dead. Brent spiked as much as 7% before settling near $78. The Dow fell more than 800 points at the lows, two days after printing a record high. And by Friday’s close the S&P 500 sat within 1% of its all-time high, volatility ended the week lower than it started, and the single largest options bet on the tape was $41 million against gold.

Hold those four facts next to each other, because together they are the whole regime in one week. A shooting war reignited in the Strait of Hormuz and the market needed two sessions to decide it did not care. In March a headline like Wednesday’s took weeks to digest. This week it took until Thursday morning, when Trump said Iran had called him looking for a deal, and the dip was gone by lunch.

But the index is hiding the bill. The S&P gained 1% on the week and the Nasdaq 1.4%, while the equal-weight index fell 0.4%, small caps fell 0.4%, and the Dow gave back 0.6%. Last week I told you the broad market was carrying the tape while the leaders rested. This week they swapped places. The megacaps and the war trade carried the week, and the average stock handed back a piece of the ground it had just recovered.

To get the most out of these market recaps and understand the framework behind my observations, I encourage you to read about my methodology here.

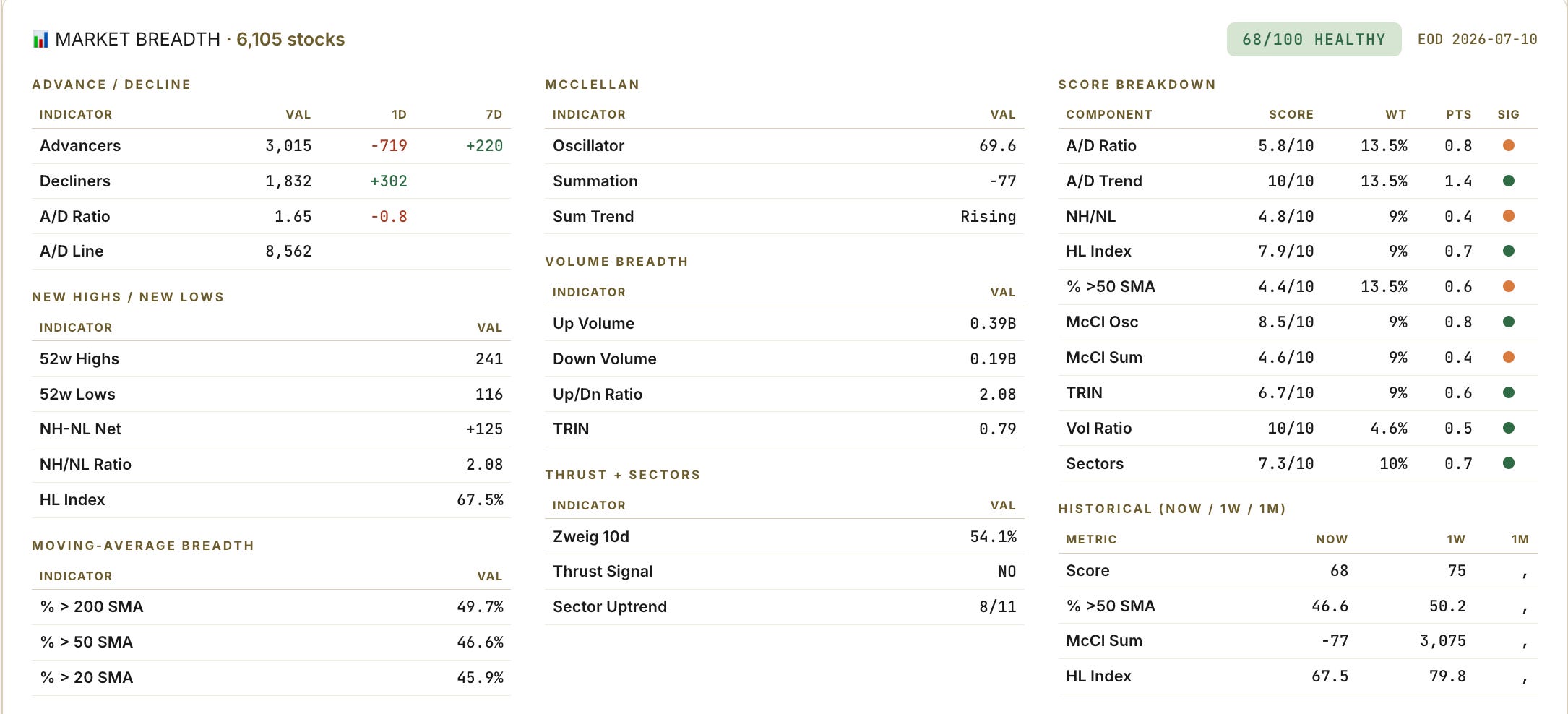

📊 Market Health

The composite health score slipped to 68 from 75, and the shape of the decline matters more than the number. Friday itself was fine: advancers beat decliners three to two, up-volume doubled down-volume, and the pressure gauge closed at a calm 0.79. The damage sits in the week’s averages, and it undoes most of what I celebrated seven days ago.

Stocks above their 50-day line: 46.6%, down from 50.2%. Above the 200-day: 49.7%, back under half after touching 54%. New highs still beat new lows, but the ratio compressed from four to one down to two to one. The high-low index eased from 80 to 67.5. Every one of those lines was healing a week ago. Every one of them gave ground.

The slow tide I keep pointing you to, the McClellan summation, tells the same story with better manners. It spent a month climbing without a pause. This week it went flat, wobbled through the strikes with the oscillator dipping negative, then turned back up on Friday. Stalled, and then it caught itself. The turn I told you I would respect never came. But this was the first week in a month the tide stopped rising, and I wrote it down.

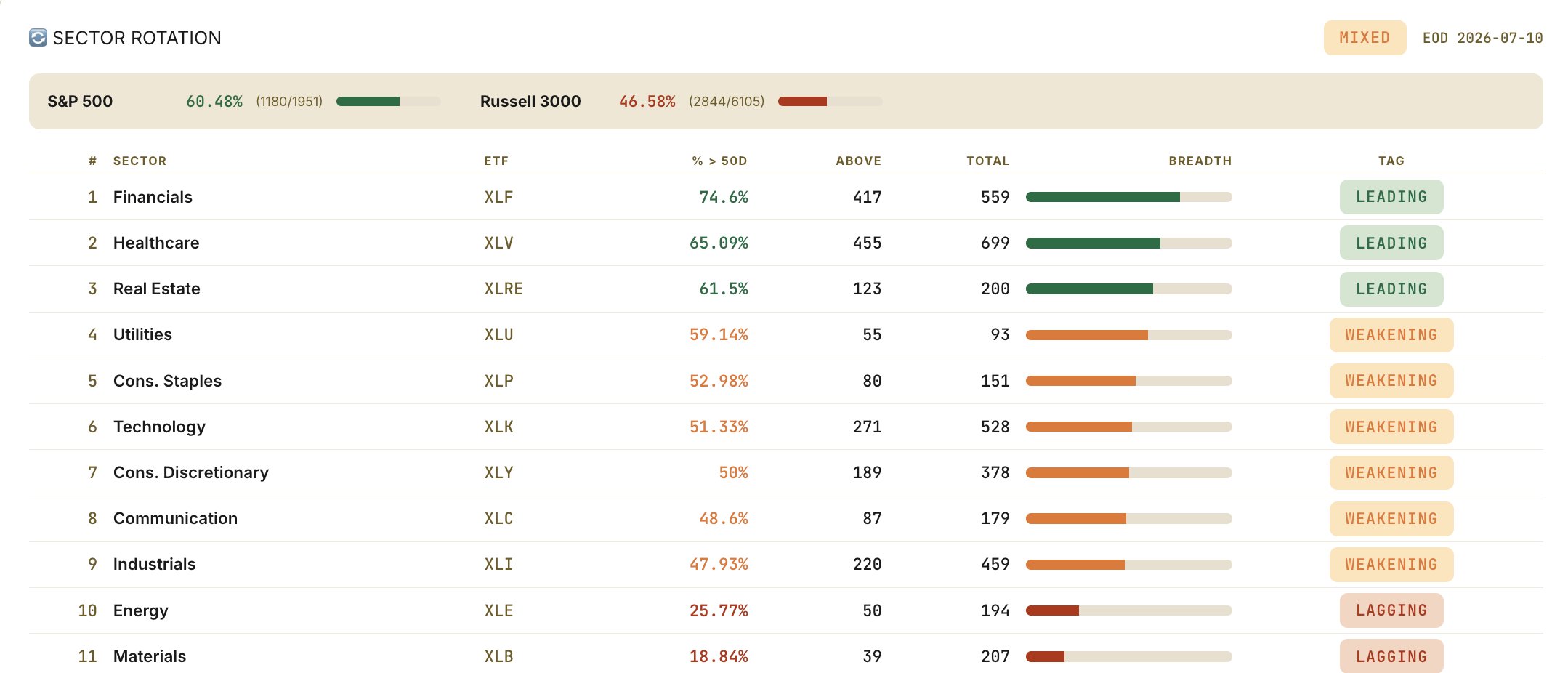

🚨 Sector Rotation

The trend board barely moved, and that is the news. Financials still own the top at 74.6% internal strength, healthcare next at 65%, real estate at 61.5%. Energy and materials are still the wasteland at 25.8% and 18.8%. Seven of eleven sectors keep majorities above their 50-day. Three weeks now, same podium. Whatever the headlines did, they did not touch the market’s internal ranking.

The week’s money argued with that board for the first time in a month. It bought the two things the trend board hates. Energy, dead last on internals, gained 3.5% as the war repriced every barrel in the Gulf. And tech, which I have spent three weeks telling you the options market was aiming at, got bought back hard: +2.3% on the week, semis +1.6% after a Tuesday session where they dropped nearly 4%. Communications rode along at +2%. Meanwhile the market sold what had been working. Staples fell 2.1%, healthcare 1.7%, industrials 1.8%, utilities 1.2%, materials 3% at the bottom of the pile.

So read the two boards together, because they disagree for an honest reason. The trend board measures what holds. The week’s tape measures what moved. What held was the financial-quality spine this rally has been built on since June. What moved was a two-day scramble into oil because of missiles and back into chips because they got cheap fast.

One follow-up. Few weeks ago I put a healthcare leader up as trade of the week betting the group would firm behind it, and last week the group showed up. This week healthcare gave back 1.7% on price while holding second place on internals, and the name itself sat flat through the mess, up almost 6% since I flagged it. Leaders that refuse to fall while their group corrects are exactly what that trade was built on.

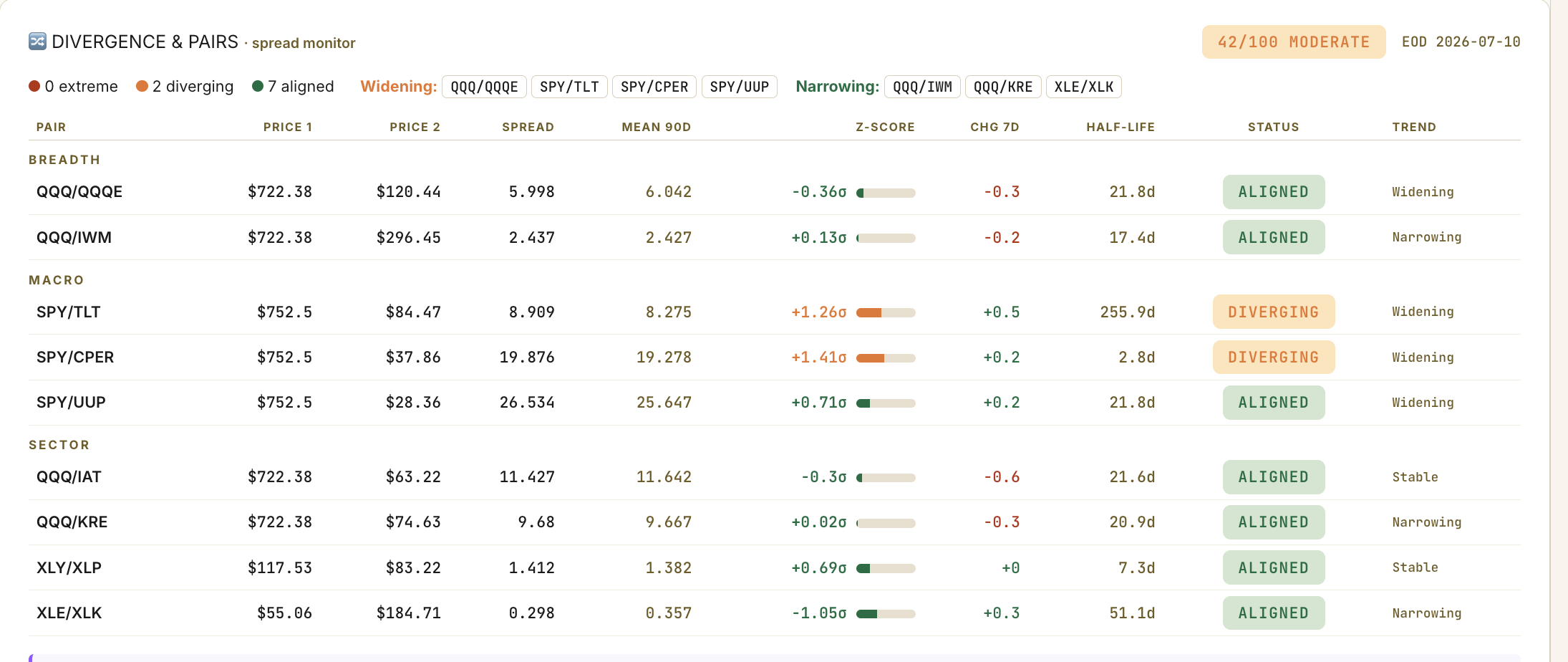

🔍 Pairs Alignment

Seven of nine pairs aligned, nothing at an extreme, and the two that are stretching both point the same direction. Stocks against long bonds is now 1.3 standard deviations wide and widening. Stocks against copper, 1.4 and widening. Equities are decoupling from both the bond market and the real economy’s favorite metal at the same time, and doing it into record territory.

The bond half of that is the one earning my attention, because this is two weeks running now. Last week Treasuries shrugged off a jobs report ugly enough to justify a rally. This week they fell again, about 1.2%, through a live shooting war. Bonds have now refused to act as a haven twice in ten days, once against weak data, once against missiles. Meanwhile look at what the tape sold: utilities, the most rate-sensitive corner of the whole board, closed red on the week even as the index climbed. Real estate held its number-three internal rank, but it sits in the same crosshairs. The bond market is telling you something is bothering it that has nothing to do with growth, and the rate-sensitive half of my leadership board is the first place that worry lands. A slow grind higher in yields is survivable. This week was slow. I am watching the speed, nothing else.

The narrowing spread is its own tell: energy against tech closed a chunk of its months-long gap this week. That was the single cheapest relationship on my board, and it took a war to start correcting it.

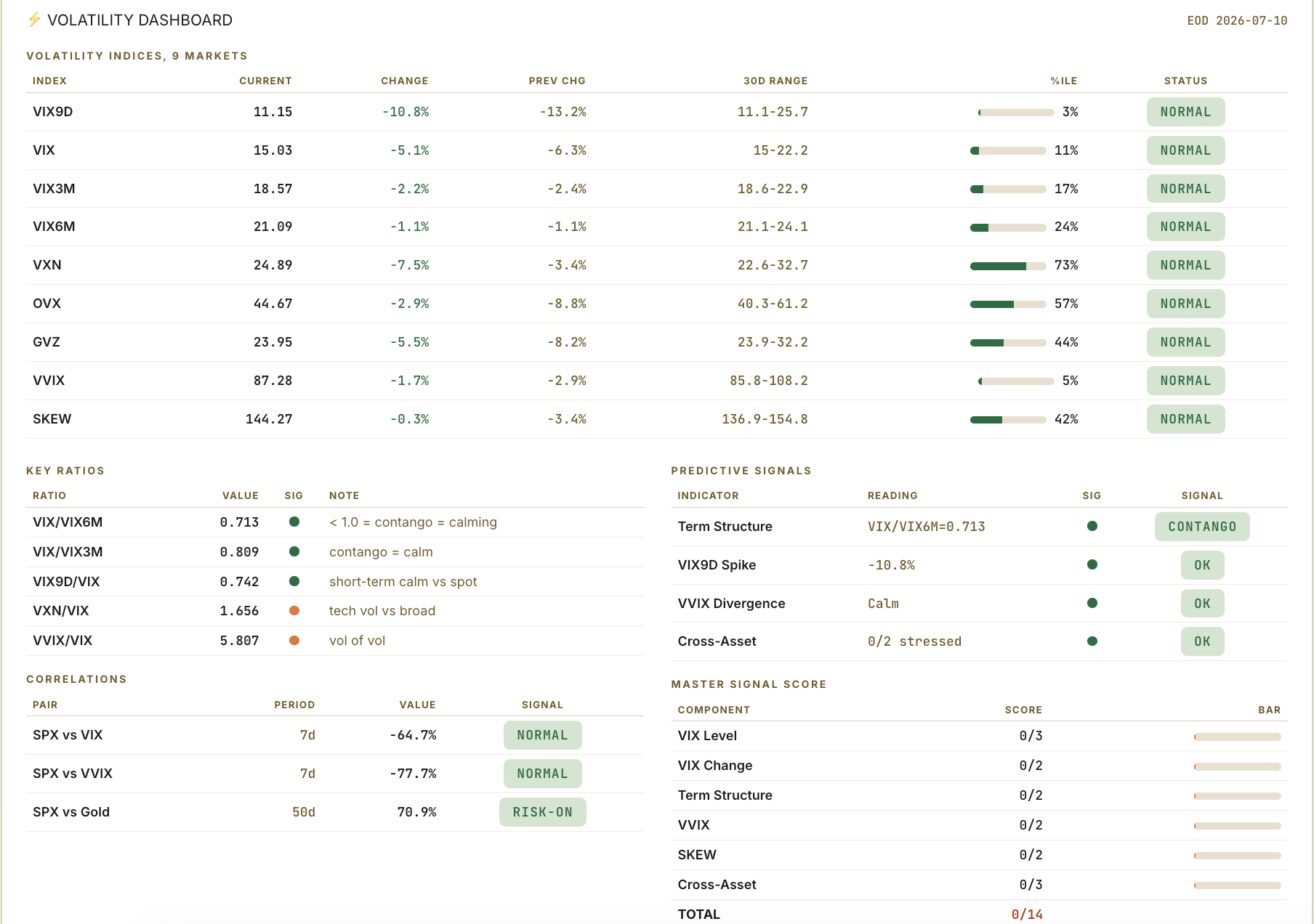

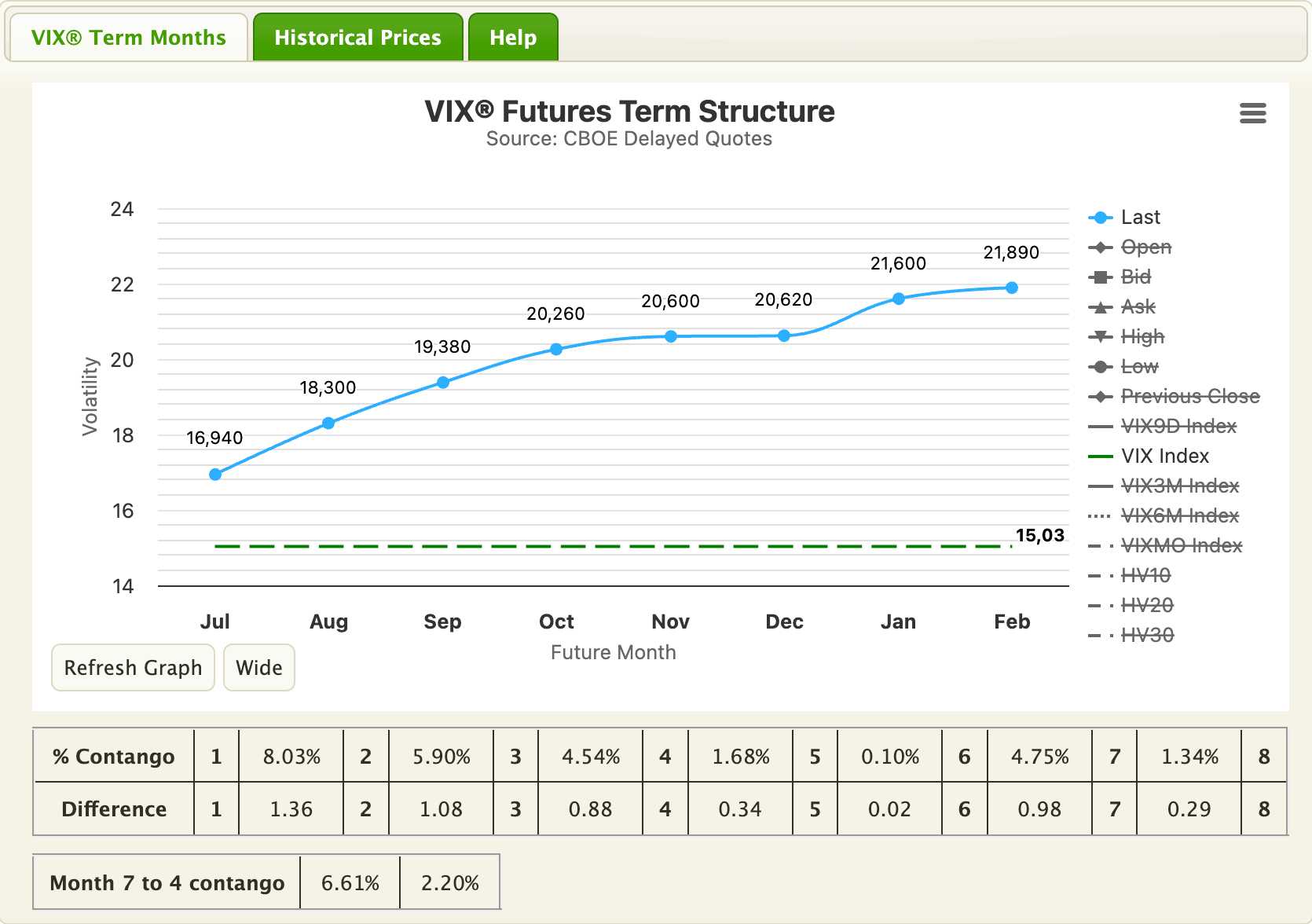

📉 Volatility

Now the board I keep rereading. The United States bombed Iran twice this week, and the VIX could not close above 17. It peaked Wednesday at 16.9, faded two straight sessions, and finished at 15.03, down 7% on the week. The nine-day gauge sits at 11, the bottom of its range. The curve never left contango. Vol-of-vol is on the floor at 87. By every broad measure, the options market watched a war restart and priced a nap.

Two corners still refuse to sleep, and they are the honest map of where risk lives. Nasdaq volatility holds the 73rd percentile of its range, the fourth straight week tech vol has been the expensive corner of the board, and Tuesday’s 4% semi flush showed you once again why that premium exists. And oil volatility now sits at 45, the 57th percentile, the one place on the entire vol surface where the war is still being paid for. Even the crash-insurance bid I flagged last week backed off: SKEW came down to 144, the middle of its range. The tail hedgers eased up during a week with actual missiles in it.

The posture stays what it has been for a month, with one addition. Broad index hedges remain a waste of premium. If you hedge equities, hedge the tech corner, which keeps demonstrating why. And if you want to own the war risk itself, the market is telling you it lives in energy vol, because that is the only place the fear still trades.

💱 FX

The currency board gave the cleanest verdict of the week, and panic did not write it. War came back and the haven bid never showed up. The franc, the first place money is supposed to run when the shooting starts, weakened about 0.3% on the week, sliding lower while stocks climbed. The yen finished flat. Gold gave back ground too. The dollar itself kept grinding, its one-month trend higher against nearly everything on the board.

Last week I gave you the recipe for real fear: the franc rising while stocks fall and vol spikes, all at once. This week we ran the live version. Missiles flew, and not one haven caught a bid, not a currency, not a metal.

🧠 My Take

Time to grade last week’s homework, and the market gave me a humbling course. I put 55% on a broadening advance. Wrong: participation shrank. I put 25% on the crowded corner cracking again, and that one half-paid, semis did drop 4% Tuesday, except the crack got bought inside 48 hours. The actual driver of the week, a restarted war, appeared nowhere on my list.

Here is what the week taught me, and it is why I run scenarios at all. The scenarios earn their keep by telling me beforehand what the market will do with whichever headline arrives, and on that count they delivered. A tape with a rising breadth tide and quality leadership absorbed a war in two days, exactly the resilience the framework said was in the price. What the framework did not promise was that the absorption would be free. The bill came out of breadth, and it is the only reason my score fell this week.

So the stance adjusts by degree. Still long. Still anchored in the financial-quality leadership, which came through the week untouched and now reports earnings from a position of strength. What sharpens is the worry list, down to two items. First, the index is a percent from record highs while less than half the market holds its 200-day; that gap either closes from below or it eventually closes from above, and nothing about this week told me which. Second, bonds that fall through both weak data and war headlines are repricing something, and they sit directly upwind of the most rate-sensitive leadership board I have had all year.

The week ahead has a real catalyst at last. JPMorgan opens bank earnings Tuesday morning, the rest of the majors follow inside ten days, and the Street expects every one of them to beat. That is the bar: the market’s strongest sector, reporting from strength, into elevated expectations.

Banks deliver and the tape broadens, 45%. Financials confirm what their internals have said for a month, participation reclaims the 50-day line, and the two-tier market heals from below. This is the base case because breadth wobbled this week without breaking, and the summation caught itself by Friday.

The war comes back for a second bite, 30%. The agreement is dead, the strikes are live, and Thursday’s entire recovery leans on one phone call the other side has not confirmed. Oil vol at the 57th percentile says the energy market is not treating this as finished even while equities do. If crude takes out Wednesday’s high, the two-day shrug gets retested, and I would expect the second scare to cost more than the first.

The index grinds while breadth bleeds, 25%. Banks are fine but not electric, no new headline, and the market repeats this week: flat-to-up index, eroding participation, until August forces the divergence to break.

🔥 Trade of the Week:

First, the book. Last week’s pick, Cadence, never gave the entry. The zone was $355 to $360, the war-week low was $365.63, and the stock closed Friday at $387, up almost 4% since last Sunday’s letter. No fill means no trade, and with earnings two weeks out I will not chase it. Discipline costs you the winners sometimes. It is still cheaper than the alternative.

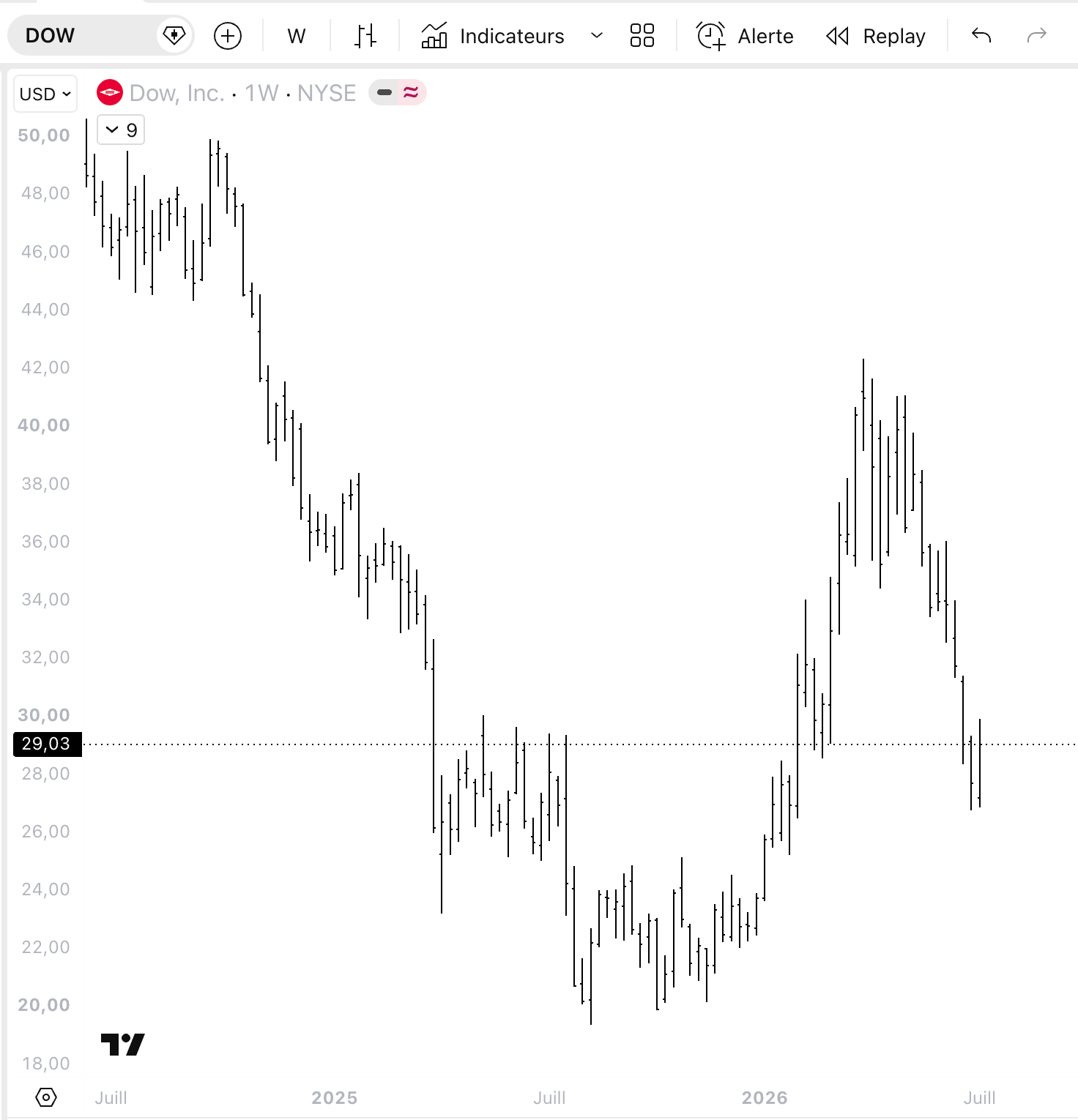

Now this week, and I am changing buckets on you. Most weeks this slot goes to a leader catching its breath. This week the better setup came out of the other end of my desk, the contrarian book, the one that goes fishing exactly where the sector board says not to look. It found Dow.

Dow Inc is one of the largest chemical producers on earth. Plastics, packaging materials, silicones, the raw inputs behind construction and autos and most of what sits on a store shelf. It is about as cyclical as a business gets, which is the entire point of what follows.

The setup

Everything you can hate about this stock is already public. Two years of industry downturn. An ethylene glut the whole street knows by heart. Weak construction and auto demand. A net loss last quarter, the dividend cut in half last summer, a credit downgrade to go with it. The stock closed the week at $29, down roughly a third from its early-2026 high near $42, and it fell there in close to a straight line, about $34 to $27 in a handful of weeks.

Here is why the level matters. That $26 to $29 band is not a random place to land. It is the zone this stock fought over for most of 2025, the ceiling it finally cleared before the run to $42. Price has now handed the entire rally back and sat down on the breakout line it launched from. This week it wicked to $27 and closed near $29. First touch from above, first bounce.

Buying cyclicals feels terrible at the moment it works. What tells you the moment may be close is when the stock stops going down on bad news, and that is what this week showed. Materials finished dead last again, down 3%, the worst sector on the board. Dow gained 3.6% against that tide. On Tuesday, with missiles in the air, someone paid $2.9 million for Dow calls against $0.4 million in puts, and came back for $2.6 million more on Wednesday. Then on Friday’s close both of my bottoming reads fired on the name at once. A washed-out price parked on a shelf that held for a year, a group everyone has left for dead, and money starting to lean the other way. That is what a bottom looks like while it forms, when it forms at all.

The honest part

Earnings land July 23, eight trading days out, and the Street expects the quarter to swing from a year-ago loss back to a real profit. That cuts both ways: a recovery is already the consensus for this print, and a washed-out stock that misses a recovery bar finds a new floor lower.

This is bottom-fishing, called by its name. The stock sits below its long-term average and the downtrend has not turned. I am betting the sector board is late, and the board is usually right longer than feels reasonable.

The dividend has been cut once already. If the cycle stays down into 2027, cheap gets cheaper, and this becomes the value trap the bears say it is.

And the week’s own theme argues against it: Dow buys its feedstock from the energy complex. A second Iran escalation that sends oil through Wednesday’s high squeezes these margins from the cost side while it scares the demand side.

The levels

Entry: around $28.70, a touch under Friday’s $29 close, or better on any drift back toward this week’s $27 low.

Stop: a close below $26.50, just under the shelf. Lose that and there is air beneath it, the next real support is the 2025 lows down in the low $20s, so a break there says the bottom thesis was simply wrong.

Target 1: $37, the congestion the stock sliced through on the way down, about 4 times the risk from entry.

Target 2: $40.80, into the supply that capped the early-2026 top, if the cycle turn shows up in the numbers.

Sizing: a starter only, smaller than usual. Earnings sit eight sessions out, so keep most of the powder for the print. If the quarter confirms, you add higher and give up the first dollar gladly.

See you next week,

Daniel

P.S. I opened the APP last week. It’s the daily version of what you just read, the same boards and screeners I run every morning before I trade.

The founding price, 50% off the first year, holds until July 19, then it goes back to full.

Disclaimer

This newsletter is for educational and informational purposes only. It is not financial advice.

The content reflects personal opinions shared publicly as a journal. Trading stocks, options, futures, or any financial instrument involves significant risk. You can lose your entire investment. There is no guarantee of profit.

The author is not a registered investment advisor, broker, or financial professional with any regulatory authority including the SEC or CFTC. Always consult a licensed financial advisor before making any investment decisions.

By reading this newsletter, you accept full responsibility for your own trading and investment choices. Past performance does not guarantee future results. Markets are unpredictable.

Screenshots are courtesy of TradingView, VixCentral, and other platforms with which the author has no affiliation. Information shared may contain errors or become outdated quickly.

This content is the intellectual property of the author. Copying or redistributing without permission is prohibited.

By continuing to read, you acknowledge and accept these terms.

Read the desk every week

Market analysis in plain English, plus the app that scans the whole US market for you.

Become a member Read the original on Substack ↗