The Money Left Tech. It Didn't Leave the Market.

Market Recap — June 28th 2026

2026-06-28 · 12 min read · Originally published on Substack ↗

TL;DR

The index sold off from the top, led by the megacap tech I flagged a week ago, while the broad market underneath rose. A cap-weighted decline sitting on top of a market that, stock for stock, finished the week green.

The rotation deepened into the corners that pay you to wait. Financials, utilities and real estate now lead outright, and technology slid to the back of the pack with energy.

Hello my friends,

Cast your mind back one week. The trend model had not read that clean in months, every index I follow was stacked above its short, medium and long lines at once, and I told you to press it on price while keeping one hand on the door. Then I told you the catch. The warning was not on the price chart. It was in the plumbing: the heavy volume that never confirmed the bounce, the leadership narrowed into the most rate-sensitive corners, and the fear in the options market bunched into megacap tech, the market’s own leadership.

This week the price came down to meet the plumbing. And it came down exactly where I pointed.

Here is the part that matters, the part the single red number on your screen hides from you. The index fell because its heaviest weight fell. Technology, the largest slab of the S&P and nearly the whole of the Nasdaq, took the week’s punishment and dragged the cap-weighted averages down with it. Underneath that, the rest of the market did not just hold. It rose. The equal-weight S&P, the small caps and the Dow all finished the week green, while the Nasdaq-100 gave back close to 5%. The broad market rose while the index fell, because the index is its biggest names, and its biggest names are tech. An average stock climbing in the same week the headline bleeds is not a market coming apart. It is the top of the market coming back to the pack.

That is the unwind I worried about last week, and it is arriving the constructive way. The danger was always that the narrow tape would resolve by the broad market collapsing toward its few leaders. Instead the leaders are mean-reverting toward the broad market.

To get the most out of these market recaps and understand the framework behind my observations, I encourage you to read about my methodology here.

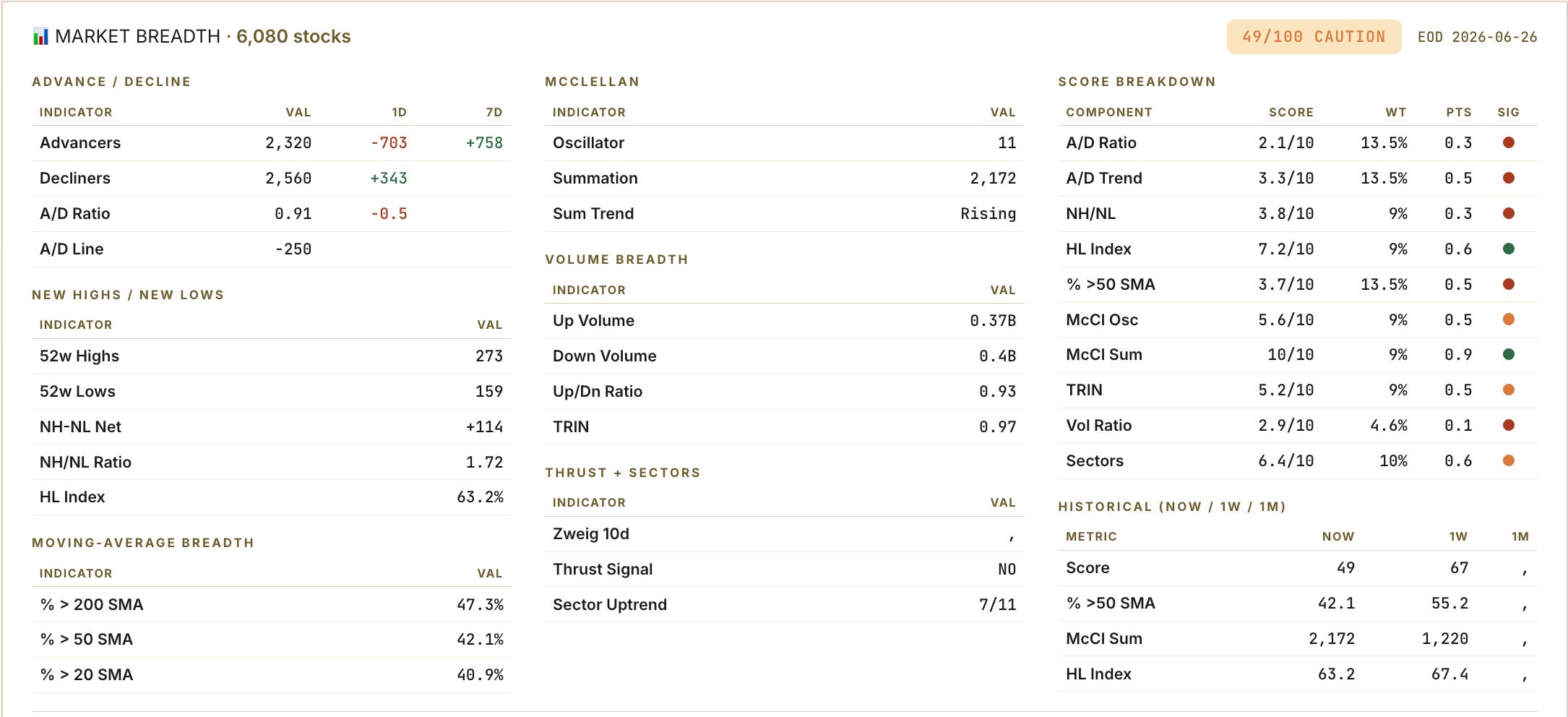

📊 Market Health

Fewer than half the market now holds its 50-day line, down from a slim majority a week ago. More names fell than rose into Friday’s close, the short-term advance-decline turned south, and the composite breadth read dropped enough to flip my dashboard from constructive to cautious. On the surface, this was a soft week.

Now look one layer down. That is where the week tells a different story. The McClellan summation, the slow tide that tracks whether breadth is accumulating or bleeding, kept climbing right through the selloff. New highs still outnumber new lows across thousands of names, if no longer by a landslide, and that is the one breadth read a handful of megacaps cannot fake. Seven of eleven sectors still hold their intermediate uptrend. The deep structure of this market did not weaken this week. It strengthened while the index fell.

Sit with that for a second. It is the whole point. A rising summation under a falling index means rotation. A top looks like the opposite. It says the selling was concentrated, money rotating out of a few crowded names while the rest of the market stayed put. The tape that worries me is the other one, the index grinding to new highs while the summation rolls over and the new-high list dries up. That is distribution dressed as strength. This week was the reverse: weakness on the screen, accumulation underneath.

So I read this as a pullback inside an advance. The kind that refreshes a tired tape rather than ending it, as long as the soft surface does not start dragging the deep breadth down with it. That is the line now. The summation is still rising. The day it turns is the day this stops being a healthy dip and becomes something I respect far more.

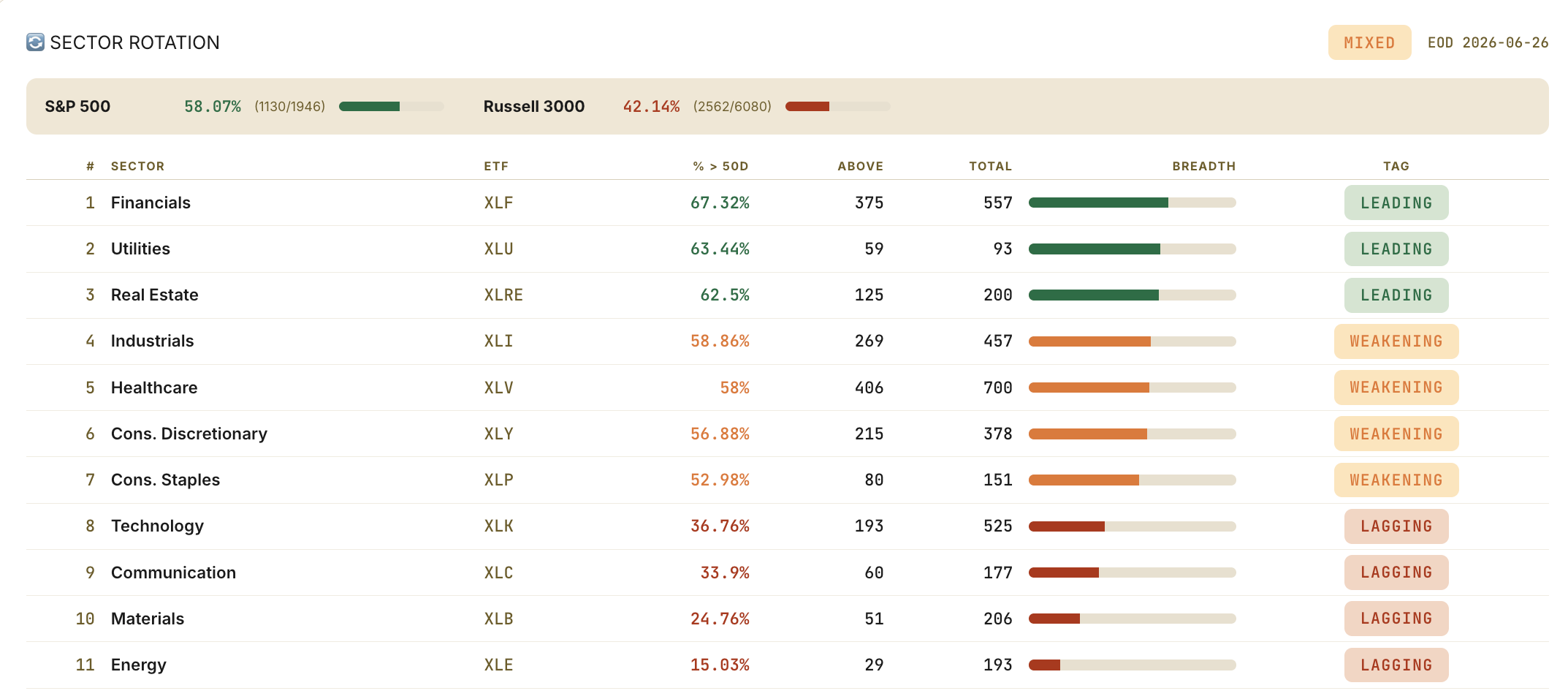

🚨 Sector Rotation

The narrowing I flagged last week resolved, and it resolved in the right direction.

Last week I told you a healthy recovery broadens off a base, more groups joining as confidence returns, and that this one had narrowed instead, the bid crowding into a handful of favorites. This week the crowd thinned the expensive names out and the leadership board reshuffled around them.

Financials lead. Utilities lead. Real estate leads. Read those three together and the message is plain: the market is paying up for cash flows, for dividends, for balance-sheet quality, for the rate-sensitive groups that win when the bond market behaves. This is the part of the tape that does well when buyers want to stay invested but stop reaching for risk.

Now read the bottom of the board. The bottom is the story. Technology dropped to lagging, with barely more than a third of its members holding their own trend. A week ago tech topped the momentum tables on a thin bench of giants. This week the bench gave way and the group slid to the back, right next to communications, materials and energy. Energy stays dead last, the single weakest group on the board, a quiet reminder that the rotation here is disinflationary at its core, a bet on rates and growth with commodities left out of the trade.

When conviction thins, money does not leave equities. It climbs the quality ladder inside them. It sells the speculative growth it bought on hope and buys the steady compounders it can hold through noise. The leadership this week, financials and utilities and real estate over technology and energy, is that ladder made visible.

One caution lives inside the good news. The groups carrying the tape, the financials and the real estate, are the most rate-sensitive on the whole board. The market has parked its money in precisely the names a sharp move in yields would punish first.

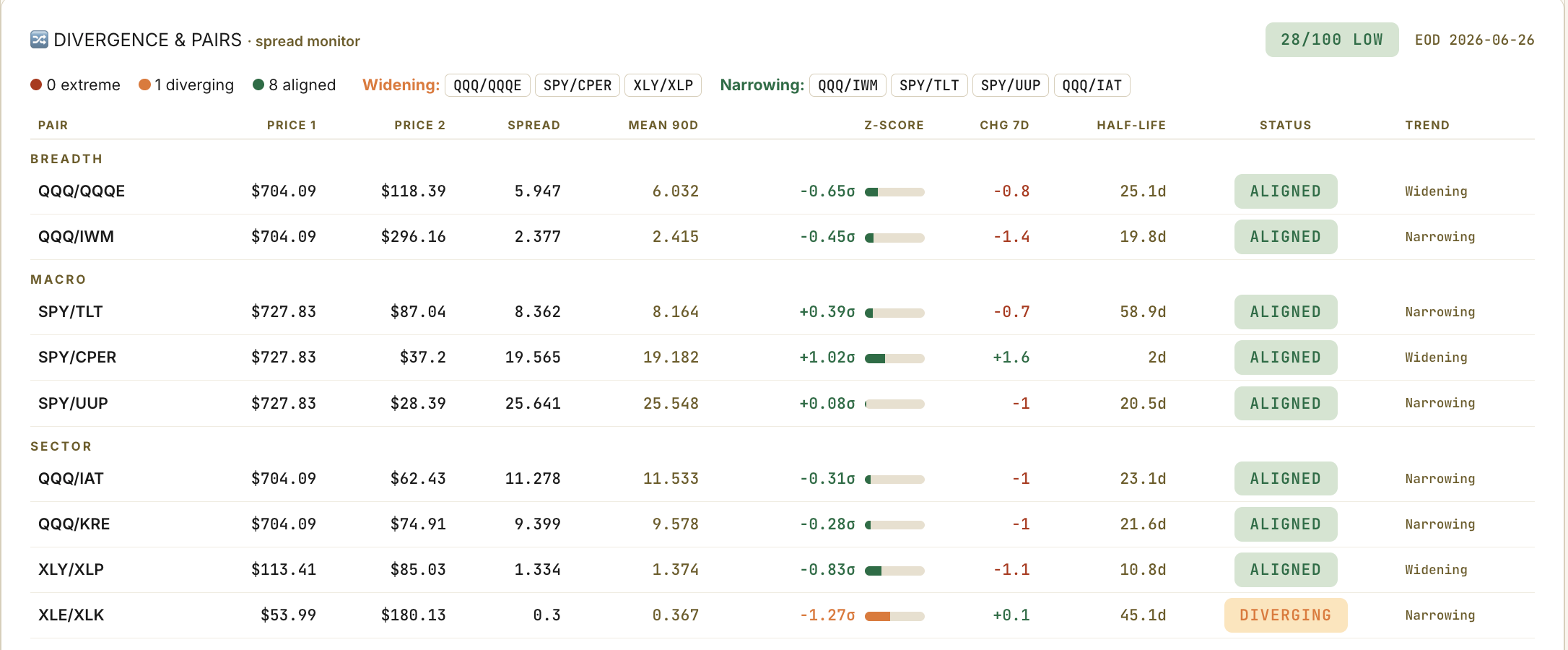

🔍 Pairs Alignment

Most of the cross-asset board is calm. The pairs I track to flag a regime change are sitting close to their normal ranges, the divergence dial reads low, and nothing is stretched to an extreme. Stocks and bonds are drifting along their usual relationship and the dollar’s move shows up cleanly without breaking anything. When breadth, sectors and spreads all tell the same measured story, it is worth trusting. This week all three say one thing: a rotation, contained.

The one relationship still pulling apart is the chronic one, energy against technology, the widest divergence on the board and the oldest. It keeps the commodity weakness honest and reminds you what kind of rotation this is. Money is rewarding rate-sensitive quality and punishing the inflation trade. The spread between the two has been telling you that for months, and this week it stretched a little further.

What I do not see is the thing that would change my posture. The selling this week was an equity-internal event, a rotation between groups that stayed inside equities and never traveled across asset classes.

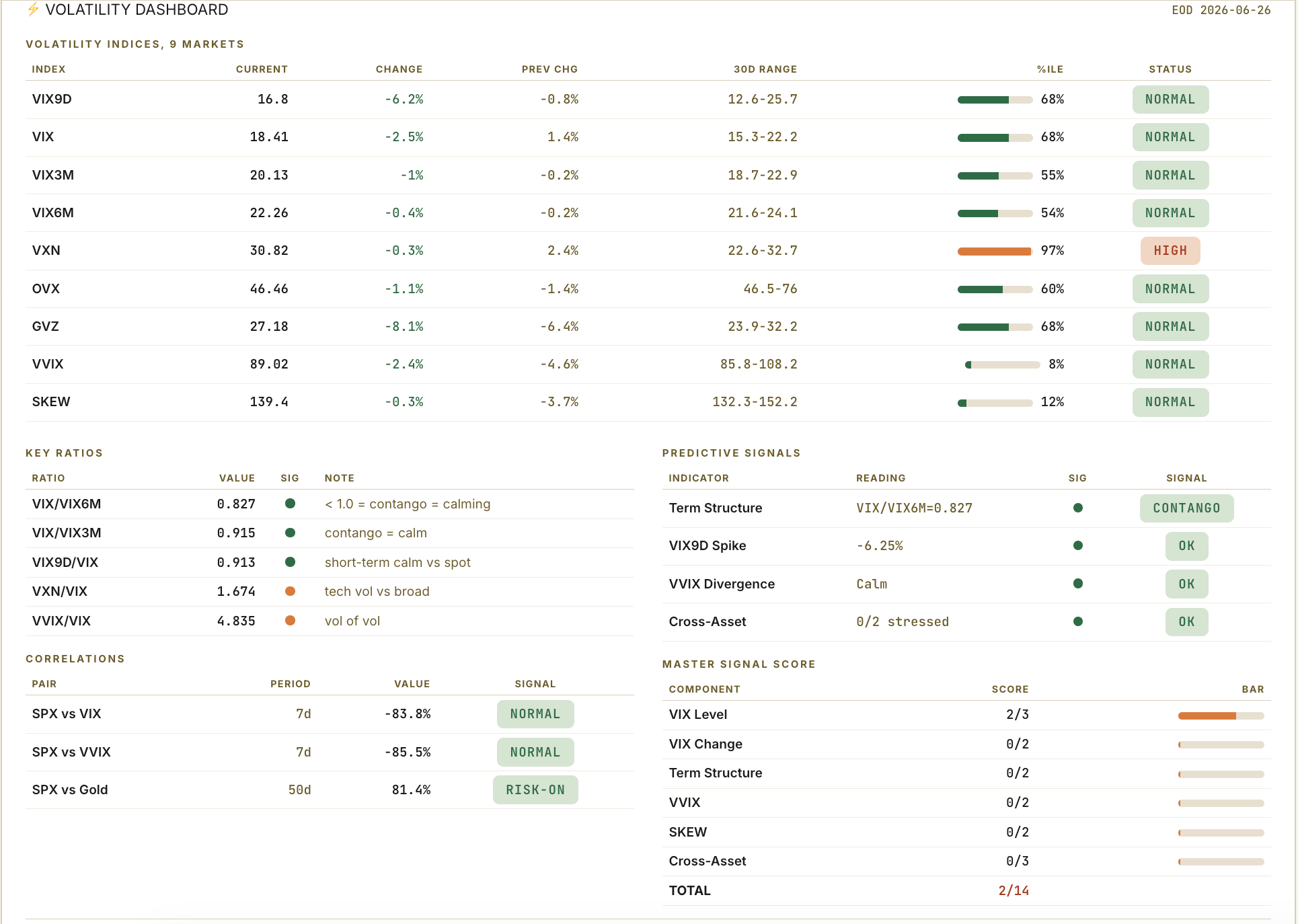

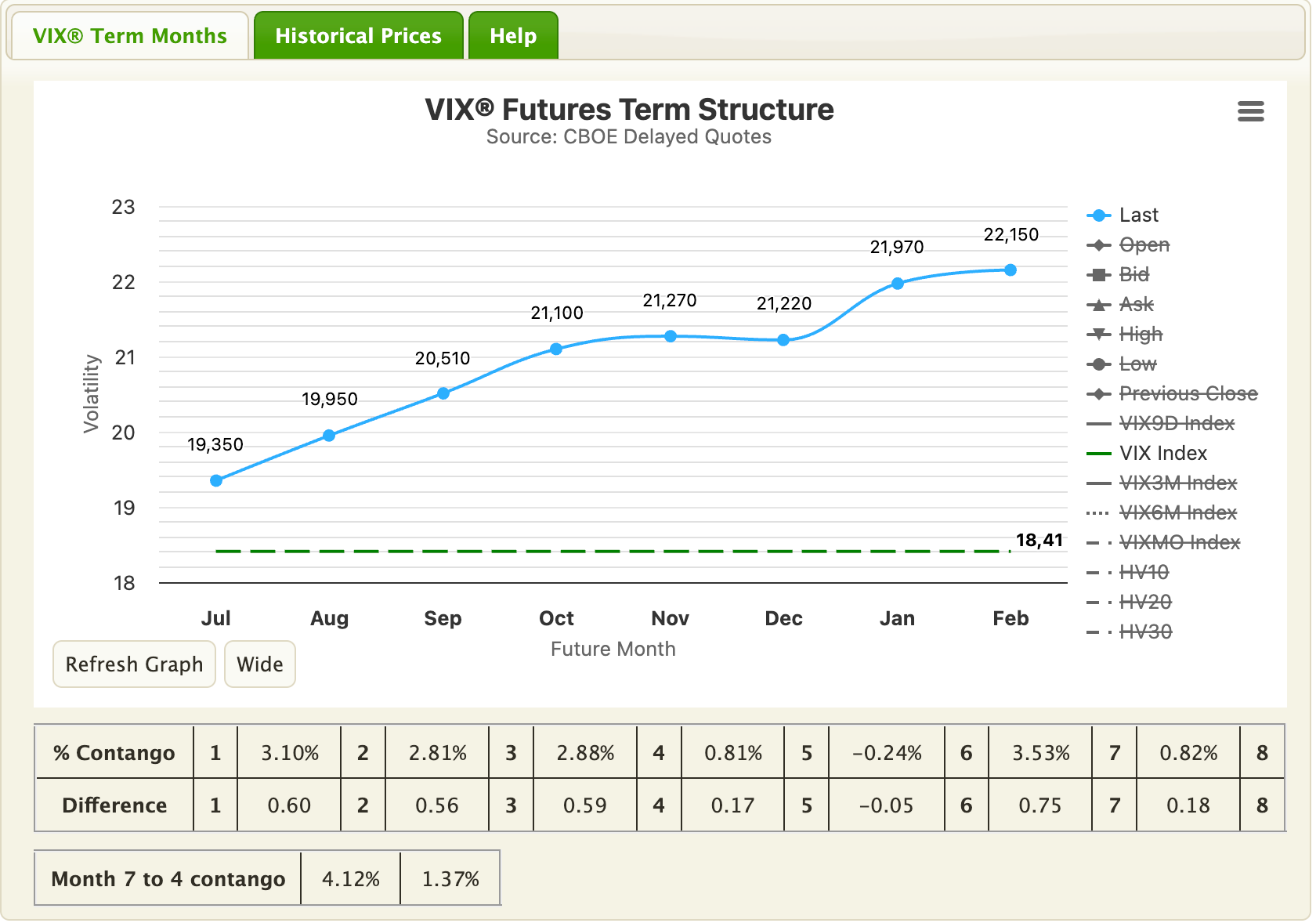

📉 Volatility

The broad volatility complex is relaxed. The curve sits in its usual upward slope, the resting state of a market that sees no spike coming, the front-month gauge holding in its normal band, and vol-of-vol is parked near the floor of its range. By the standard reads, the options market is not bracing for anything.

The exception is the one that counts, and it is the same one I pointed at last week. Nasdaq volatility sits near the very top of its range, the only gauge on my board flagged elevated, and it trades rich against the broad market. Read that next to the price action and the picture closes neatly. The options market spent last week telling you the fear was concentrated in megacap tech. This week megacap tech is the thing that fell. The nervous corner was the corner that broke. That is no coincidence. It is the options market doing its job a week ahead of the tape.

So the signal stays narrow and it stays specific. You do not hedge the index off this screen, broad vol is calm and cheap and pricing in nothing. If you hedge anything, you hedge the tech concentration, the single spot that has now shown strain on the chart as well as in the options.

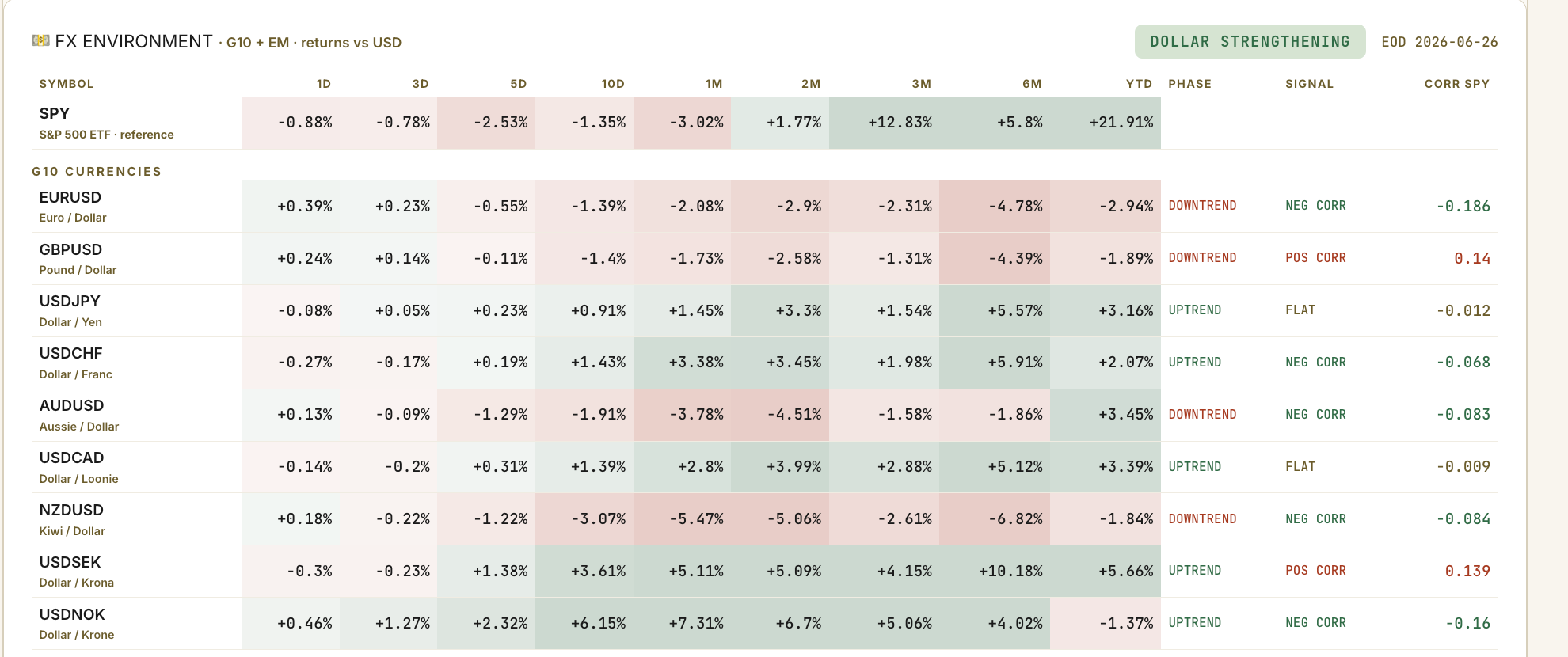

💱 FX

The dollar firmed again, a third week of quiet strength, and the move is broad. It shows up against the yen, the franc and the commodity currencies all at once, the kind of move that comes from a market reaching for dollars rather than one currency falling apart. The Australian and the Kiwi, the cleanest growth-sensitive currencies in the group, are sliding, and that lines up exactly with the energy and materials weakness on the sector board. The disinflation trade is showing up in FX too.

The yen keeps weakening, parked on the soft side, and that keeps the carry trade dormant. It is still the largest single fault line in global markets, the spring that snapped everyone to attention months back, and it still has no near-term trigger now that the Bank of Japan is behind us. Dormant is the right word.

The franc is the one I keep a finger on, the cleanest safe-haven in the group and the first place real fear shows when funding tightens. It stayed soft this week against a weak euro, and that is the tell that keeps me constructive. A firming dollar with a soft franc is risk dialing down in an orderly way. The day the franc turns higher is the day this rotation risks becoming something colder. Not this week.

🧠 My Take

The pullback I told you to expect arrived, in the corner I told you to watch, and it came the constructive way. I am not leaning bearish into a tape where the deep breadth is still rising, the new-high list still leads, and the selling stayed walled inside the most expensive part of the market. I stay long, and I lean into the quality leadership the rotation is paying for.

The caution is the same caution, only sharper. The surface breadth softened this week, the leadership sits in the most rate-sensitive groups on the board, and the options market is still pointing at tech. Last week those were warnings. This week one of them came due. The job now is to watch whether the soft surface stays walled off or starts leaking into the structure underneath.

Here is how the week ahead breaks down.

The orderly path, base case, around 50%. The deep breadth holds, the summation keeps rising, and it pulls the soft surface back up behind it. The rotation does its work, the expensive leaders finish mean-reverting toward the pack, and the broad market that rose this week takes the baton. The breadth backs this one, and it is the path a rising summation usually buys.

The spread, the real risk, around 30%. The tech weakness stops being contained. The nervous Nasdaq vol bleeds into the broad market, the soft surface starts pulling the deep breadth down with it, and the rate-sensitive leaders that carried the tape take the first and hardest hit, exactly because they led on the way up. This is the scenario the tech hedge exists for, and the one I am watching the summation to rule out.

The stall, around 20%. Nothing resolves. The volume stays absent, the surface cannot firm and the deep breadth cannot break, and the tape chops sideways under its highs until the next catalyst gives it a reason to pick a side.

I am long, tilted toward the quality leaders the rotation is rewarding and away from the speculative growth and the commodity laggards. I carry a little downside insurance aimed at the tech concentration, the one corner that has now shown strain everywhere I look. The posture has not changed since last week.

🔎 Options Flow: Smart Money Positioning

The flow tilted bearish on the week, more downside bets than upside. The biggest tickets were not subtle about where they pointed. Heavy puts hit the crypto miners, the high-beta names that run hottest when the tape is loose and bleed first when it tightens, and more puts landed on the emerging-market complex, the part of the world a firming dollar squeezes. When the most speculative money buys protection on the most speculative names, it is telling you it sees the same rotation the sector board is showing.

It was not all defense. A couple of upside bets went into semis and into Taiwan, a reminder that even in a defensive week the conviction in the chip cycle has not died. It has just gone quiet. But the weight of the flow sat on the bearish side, concentrated in exactly the corner this letter has been wary of for two weeks.

Put it next to everything else and the message holds together. Breadth says rotation. Sectors say quality over speculation. Vol says the fear lives in tech. And now the flow says the fast money is paying up to protect the frothiest names. Four screens, one story. Lean long, stay in the leaders, and keep the exit in sight on the speculative stuff.

🔥 Trade of the Week:

A quality leader now pausing inside a strong uptrend.

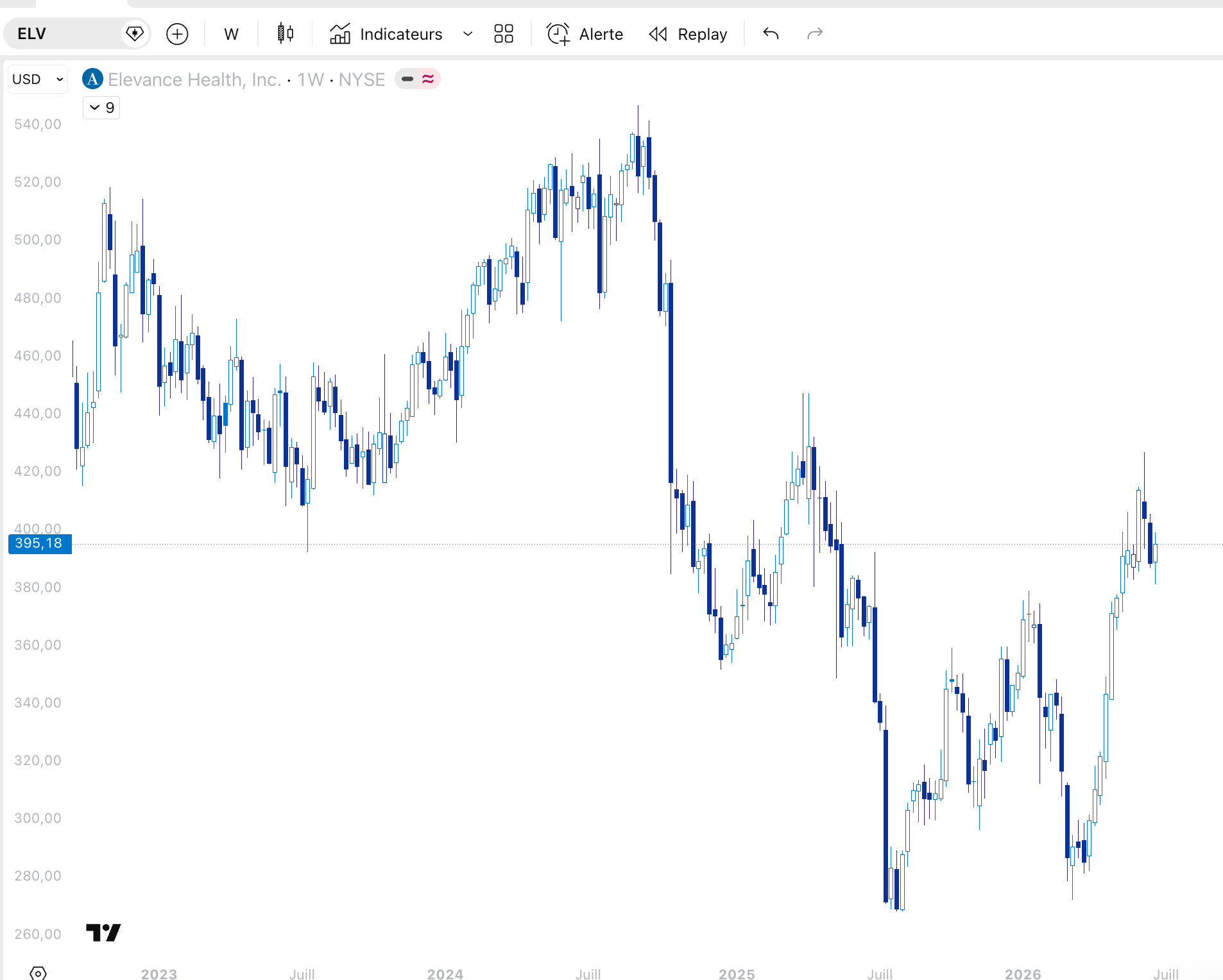

Elevance is the kind of name this rotation is built to reward. It is one of the big managed-care insurers, a durable compounder with the sort of cash flows that do not blink in a soft quarter, and for a long stretch it was the stock nobody wanted. Then it woke up. It climbed better than 30% over the past quarter while healthcare as a group went flat, and that is the definition of a leader, a name dragging its whole neighborhood behind it.

Here is why it earns the slot this week over a momentum name printing fresh highs. ELV ran hard, then stopped to breathe. It has drifted sideways for a month, eased back about 9% from its high, and this week it held flat while the index sold off around it. That is a chart asking for an entry. You are not chasing a breakout. You are buying a strong name on the dip the rest of the tape just handed you.

The case is the rotation. When the market sells the speculative and buys the durable, you want to own the durable names on the days they pull in. ELV is durable, it leads its group, and it is pulling in. The flat week while the Nasdaq bled is the whole tell. This is exactly the kind of name the money leaving tech is looking for a home in.

Now the honest part. Healthcare as a group still reads as weakening on my sector board, so you are buying a leader inside a soft neighborhood, and a leader can only carry a weak group so far. The entry sits a touch below where it trades now, so let the dip come to you rather than reach for it.

Entry around 379, on a pullback toward the base of the range. Stop a close below 358. Target 424, the prior high.

See you next week,

Daniel

Disclaimer

This newsletter is for educational and informational purposes only. It is not financial advice.

The content reflects personal opinions shared publicly as a journal. Trading stocks, options, futures, or any financial instrument involves significant risk. You can lose your entire investment. There is no guarantee of profit.

The author is not a registered investment advisor, broker, or financial professional with any regulatory authority including the SEC or CFTC. Always consult a licensed financial advisor before making any investment decisions.

By reading this newsletter, you accept full responsibility for your own trading and investment choices. Past performance does not guarantee future results. Markets are unpredictable.

Screenshots are courtesy of TradingView, VixCentral, and other platforms with which the author has no affiliation. Information shared may contain errors or become outdated quickly.

This content is the intellectual property of the author. Copying or redistributing without permission is prohibited.

By continuing to read, you acknowledge and accept these terms.

Read the desk every week

Market analysis in plain English, plus the app that scans the whole US market for you.

Become a member Read the original on Substack ↗