The Top Got Postponed.

Market Recap — May 31th 2026

2026-05-31 · 12 min read · Originally published on Substack ↗

Hello my friends,

I have been cautious for weeks, and I still hold the heaviest cash position of my year. But the job every weekend is to read the tape without my bias, and this week the tape moved, meaningfully and mostly in one direction. The index did not roll over into the double top I had been watching; it broke through the February high to fresh records at 7,580. The war premium that kept Brent above $100 with the Strait of Hormuz closed came out of the market fast: oil fell fourteen percent on the month as a US-Iran arrangement moved from rumor toward something real. And the breadth that sat dead flat last week ticked up. So this week I am going to do what I always say I will, which is follow the data where it leads, even when it leads away from where I have been parked.

The summary up front: the constructive case strengthened this week, and several of my reasons for caution quietly went away. What is left on the bearish side is narrower and slower than it was. No longer a war or a double top, but the more patient risks of concentration, complacency, and a Japanese yen still loaded one candle from its line.

Now, layer by layer, what the data is saying.

To get the most out of these market recaps and understand the framework behind my observations, I encourage you to read about my methodology here.

📊 Market Health

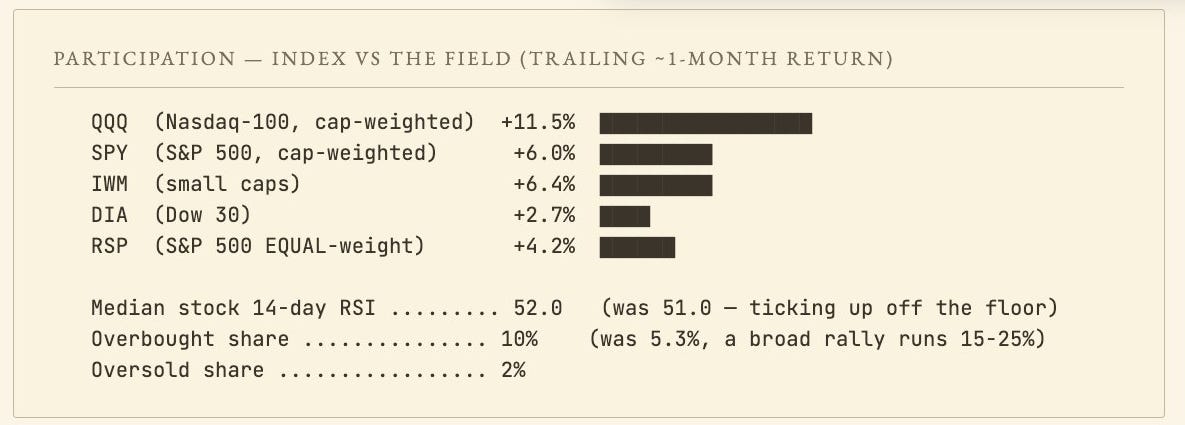

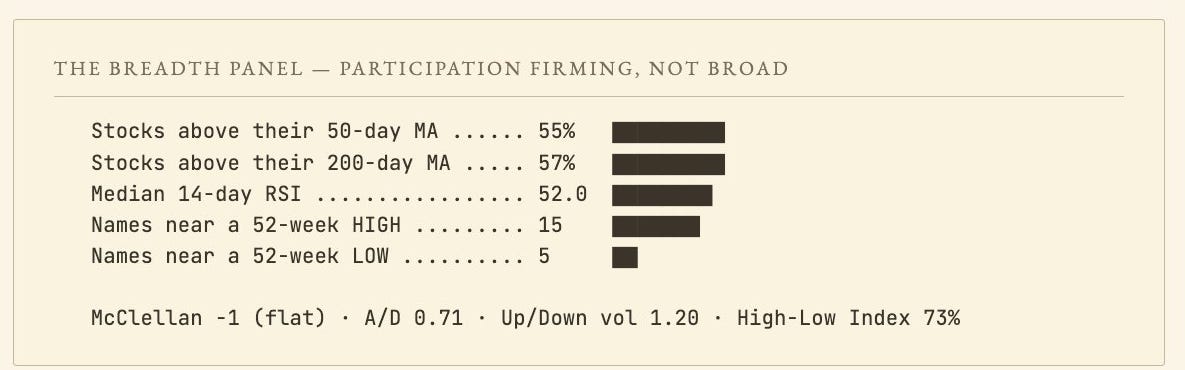

Last week the median 14-day RSI across my universe sat at exactly 51.0. Dead, flat, perfectly asleep. This week it ticked up to roughly 52. That is not a stampede, but it is the first time in a month the needle moved in the right direction rather than sideways. More telling: overbought readings rose from 5.3% of the universe to 10%, and the proportion of stocks holding above their 50-day moving average firmed to 55%, with the 200-day line at 57%. A broad rally usually carries 15% to 25% overbought, so the field is firming, not yet broad. The field is not awake. But it is no longer comatose, and that is a real change from the flat-line I described to you a week ago.

Here is the tension that still defines everything. QQQ is up 11.5% on the month. Equal-weight (RSP) is up 4.2%. That gap did not close as the field improved. It widened, from about six points last week to better than seven now. So we have two things happening at once that I have to hold in my head simultaneously: the broad field is marginally healthier than it was, and the leadership is marginally more concentrated than it was. A market can broaden and narrow in the same breath, and right now it is doing exactly that.

The crack I have been waiting for, index at new highs with internals deteriorating and leadership stumbling, did not arrive this week. We got the new highs. The internals stopped deteriorating and quietly improved. And the leadership did not stumble; it accelerated. That is the opposite of the three-part topping configuration I described last week. I have to be honest about that, because the whole point of doing the work is to let it overrule my prior.

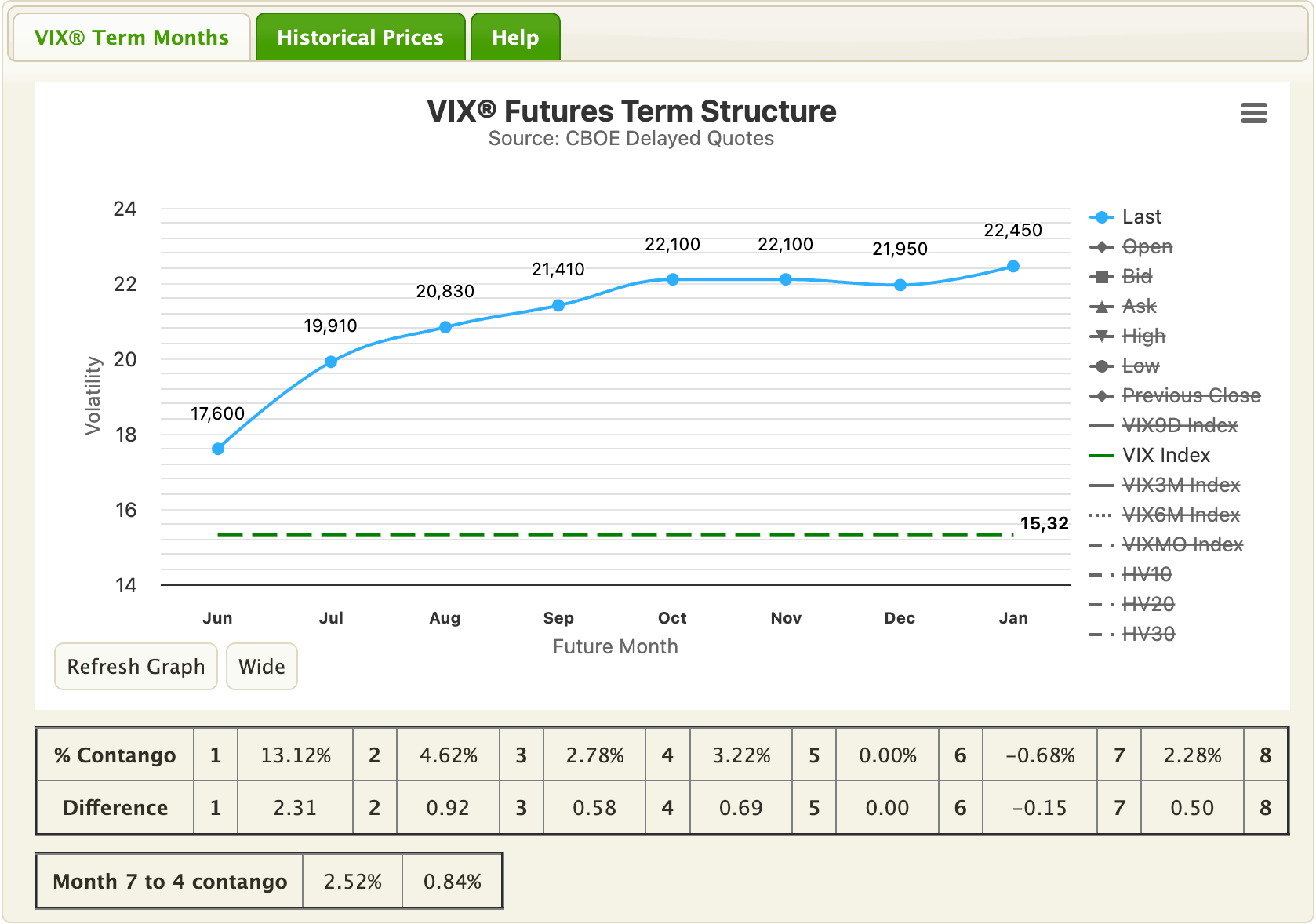

📉 Volatility

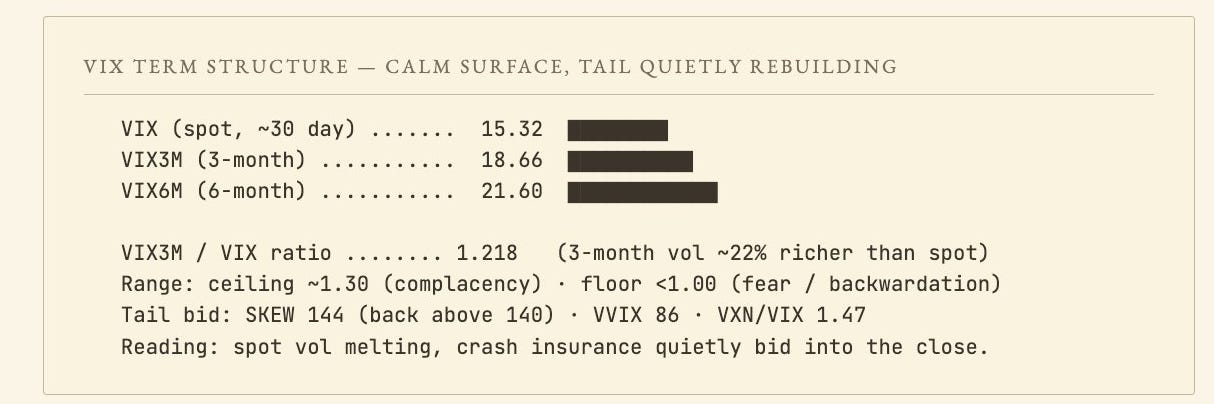

The VIX closed at 15.32, down again from 16.70 last Friday and 18.4 the week before. Three straight weeks of compression. On the surface, deepening calm, and calm is what precedes tops. The VIX3M/VIX ratio, my complacency gauge, closed at 1.218, up from 1.199. It works like this: the higher it climbs, the more complacent the market; the ceiling where tops historically form sits around 1.30. We are not there yet, but we are grinding toward it, one quiet week at a time.

And here is the one number that does not fit the calm. SKEW jumped to 144.2 on Friday's close, up from 139.5 the day before and back above the 140 threshold I watch, near the elevated readings of mid-May. That is the tell. The VIX measures the price of at-the-money fear; SKEW measures the price of tail protection, the cost of insuring against the big left-tail move. So while spot volatility melted to a three-week low, someone was quietly paying up for crash insurance into the weekend. VVIX held in the mid-80s. Read together, the picture is more two-faced than last week: the surface is calm and getting calmer, but underneath it the tail bid is rebuilding rather than cooling. My triad to watch: VVIX pushing higher, SKEW reclaiming and holding above 140, and the VIX3M/VIX ratio grinding up toward the 1.30 complacency ceiling. All three describe the same thing, a calm surface with fear building underneath it. This week SKEW is the one that lit, back through 140, while the ratio keeps climbing toward that ceiling and VVIX sits quiet in the mid-80s. It is the first wisp of smoke, well short of a fire alarm, and it is the part of this week's tape that keeps my hand near the exit even as the rest of the data pulls me back in.

🔍 Pairs Alignment

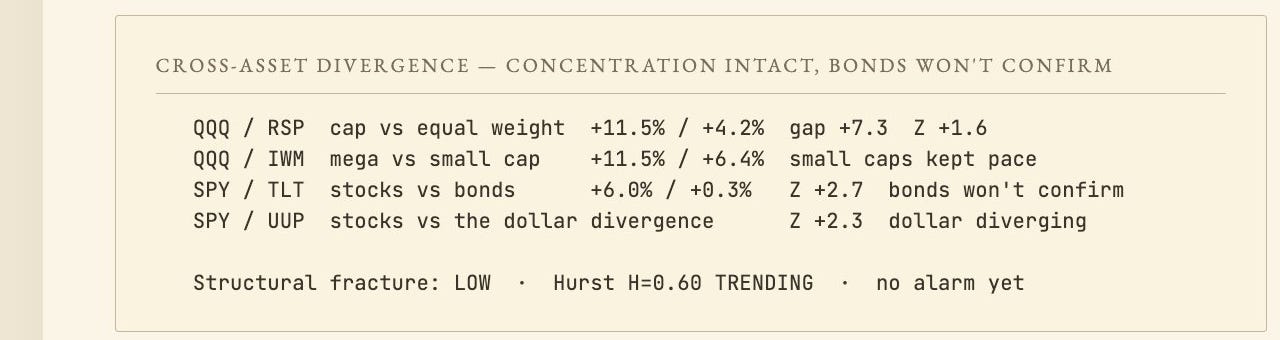

QQQ vs equal-weight. The purest concentration read, and it got more extreme, not less. QQQ rode a near-twelve-percent month; strip the mega-caps out and the equal-weight S&P is up barely four. The engine of this rally is still a handful of names.

QQQ vs IWM. Here is the crack in my thesis. Small caps were up 6.4% on the month. They actually kept pace with SPY and beat equal-weight. For two months I have told you small caps were lagging relentlessly, and that the soft-landing trade was being expressed in mega-cap tech and almost nowhere else. This month, the most rate-sensitive, most domestically-geared corner of the market participated. That is a small but real vote for broadening, and I will not pretend I didn’t see it.

Stocks vs bonds. The one that still nags. The twenty-year Treasury proxy is essentially flat on the month, refusing to follow equities higher. The bond market has now spent the better part of two months pricing a materially different path than the stock market. When two enormous liquid markets disagree this persistently, I have learned to bet on the bond market being right. Bonds are run by people paid to be paranoid, stocks by people paid to be optimistic, and in a standoff paranoia has the better record. This is the pillar of my caution that survived the week fully intact.

🚨 Sector Rotation

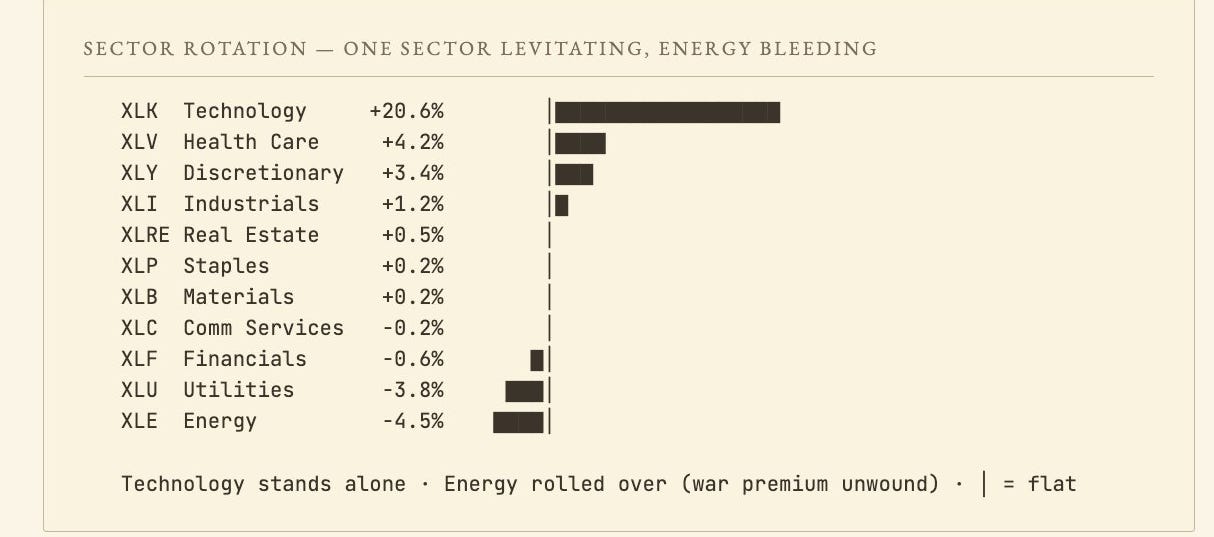

Technology is up just over 20% on the month, even more dominant than the thirteen percent I flagged last week. The number-two sector is now Health Care at under five percent. But look at the bottom of the table, because that is the story. Energy is down 4.5% on the month. Last week Energy was the only non-tech sector with a genuine pulse, levitating on a war premium with Hormuz closed and Brent above $100. This week it rolled over and bled. This is bigger than a rotation inside the table. It is the unwinding of the entire geopolitical risk trade that I told you was the biggest mispriced macro overhang in the market.

I have to connect this to the news, because the two are the same event. The rumors I mentioned last week, a US-Iran arrangement involving uranium-stockpile surrender and a reopening of the Strait, appear to be moving from rumor toward reality. Oil voted before the headlines confirmed it: WTI fell to roughly $88, dragging the whole oil complex down fourteen percent on the month. And here is the part that matters for everything else: falling energy is a tax cut for every other sector’s margins. The inflationary impulse I was worried would pressure the rate path is deflating in real time. The bear case that ran war → oil spike → sticky inflation → no rate cuts → equities lower just had its first domino pulled out. I cannot keep citing an oil-shock risk that the tape is actively pricing away.

The Discretionary-versus-Staples read rounds it out and leans gently constructive: Discretionary (+3.4%) is now pulling ahead of Staples (+0.2%), the modest fingerprint of a consumer trade that is leaning offensive rather than defensive. A month ago both were jammed together at the bottom. Small change, right direction.

💱 FX

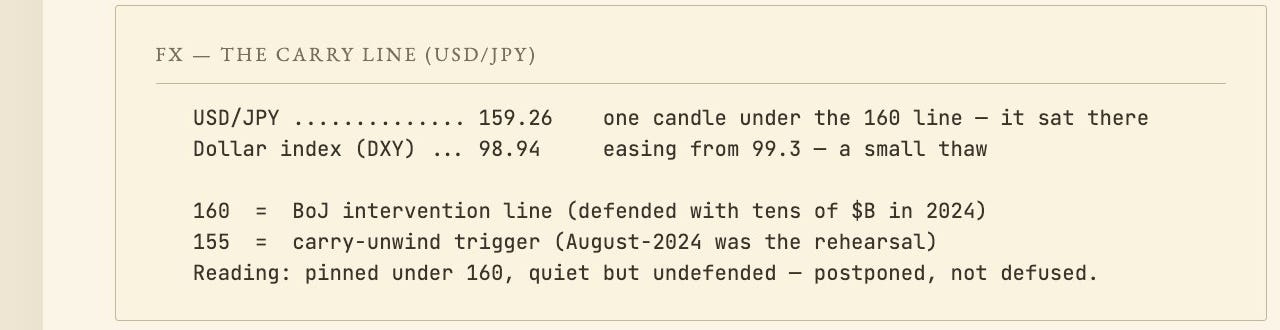

I have said for weeks that the single most important chart in the world is USDJPY, not any equity chart. It closed the week at 159.26, essentially unchanged from 159.16 last Friday. One good candle from 160, and it simply would not move. The most concentrated single point of failure in a concentrated market spent the week perfectly quiet.

The mechanism is unchanged. You borrow yen at near-zero, convert to dollars, buy higher-yielding US assets, increasingly mega-cap tech, where the momentum and the liquidity live. As long as the BoJ stays quiet and the yen drifts weak, the trade prints on two fronts. My working hypothesis remains that this cheap-yen funding is one and the same trade as the equity concentration you see in the sector table, two faces of one trade rather than two stories. The 160 zone is where Tokyo has historically turned from rhetoric to intervention; they spent tens of billions defending it in 2024, and officials have signaled again they will act against excessive volatility.

The asymmetry is what I keep close. If USDJPY pushes through 160 without intervention, the carry trade rebuilds and the mega-cap bid gets another tailwind. That is the bullish path, and it would extend exactly the concentration we already have. But a break back down through 155 is the line where I treat the carry-risk regime as live: funds that borrowed cheap yen would have to sell US assets to repay loans suddenly more expensive in dollar terms. August 2024 was the rehearsal. A modest BoJ hike produced one of the most violent short-lived dislocations in years. Meanwhile the dollar itself eased to 98.9, down from 99.3, a small thaw that slightly loosens the strong-dollar grip. So 159 is still the number I go to bed thinking about. It did not move this week. It also did not defuse.

🧠 My Take

The dashboard still tells two stories, but the weight between them shifted this week, and I am not going to pretend it didn’t.

The cautious story. Concentration is more extreme, not less: tech alone at +20%, the QQQ/equal-weight gap wider than ever. SKEW broke back above 140 to 144, a calm surface over a rebuilding tail bid. Bonds still refuse to confirm the rally after two months. And USDJPY sits one candle from the line, quiet but loaded. That is a coherent, patient bear case. But notice what it no longer contains: no war, no oil shock, no double top. The three loudest, fastest catalysts I was watching all resolved the other way this week.

The story my bias does not want to write. The index broke out to new highs instead of failing at the February level. Oil came off and took the inflation-shock risk with it. Breadth ticked up rather than rolling over. Small caps kept pace. The VIX compressed for a third straight week. I had flagged the war and the double top as the catalysts that could tip this tape lower, and both went the opposite way. When the catalysts you were watching for fire in the other direction, the data is telling you something, and the discipline is to update the positioning rather than keep narrating the old thesis.

So here is where I sit. I am not chasing mega-cap tech at full stretch. Leaning into a concentration rally at the highs is how you get carried out the other way. But I am beginning to put cash back to work, selectively, on names that have already corrected hard. The shopping list stops being homework and starts being a portfolio, one careful position at a time.

Constructive (~55%). The breadth thaw continues, equal-weight closes the gap, the Iran de-escalation holds and keeps oil falling (WTI in the $80s or lower), and AI-infrastructure names confirm that the capex is real and monetizing. The field joins the leaders, and this resolves into a broad bull.

Cautious (~45%). USDJPY finally breaks 160 the wrong way and the carry unwinds; VIX3M/VIX tags 1.30 while SKEW stays bid above 140 (it just reclaimed it Friday at 144); bonds force the rate question back open. That cluster turns concentration-hedging into contagion-hedging fast. The single point of failure has not been defused, only postponed.

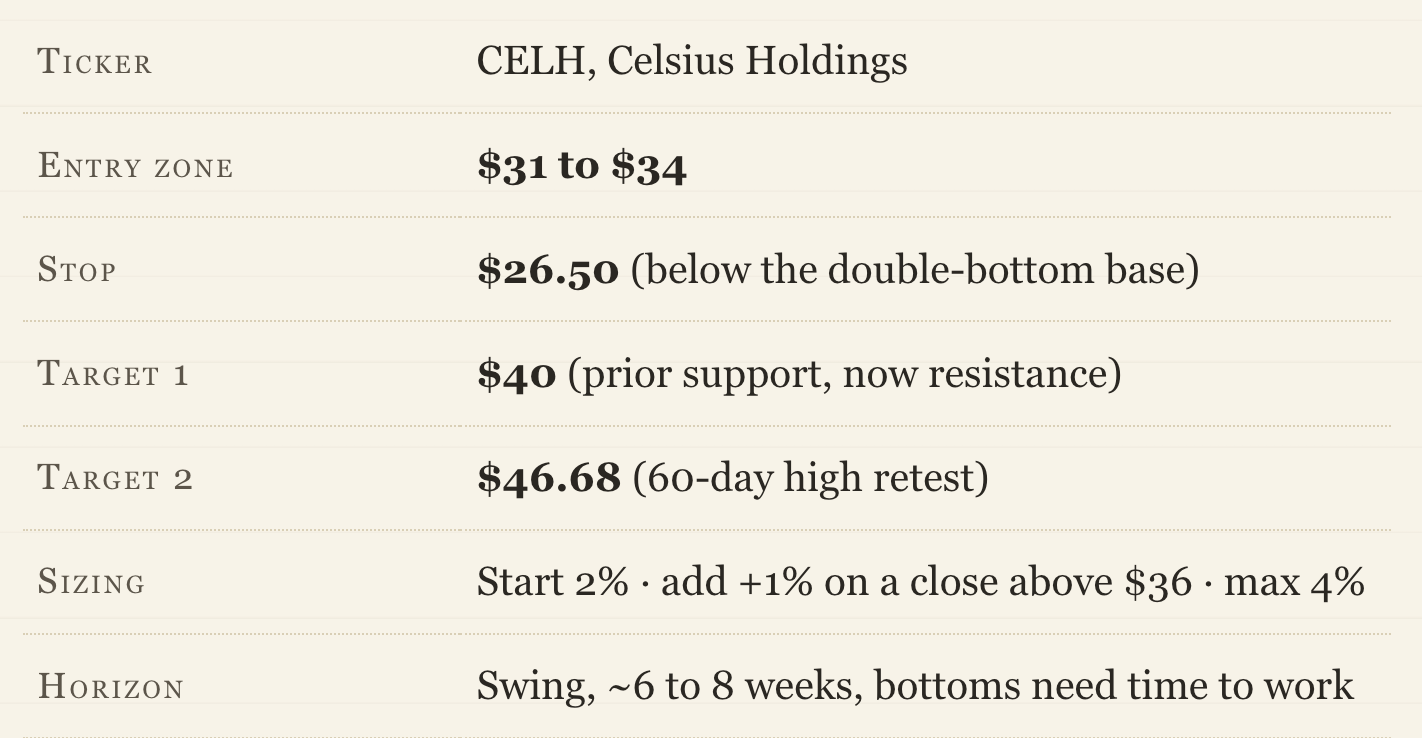

🔥 Trade of the Week:

I will say it before the trade, same as always: my caution has softened but not vanished, and I am not abandoning discipline for a single name. But my screeners flagged a setup I respect, and it fits the entire letter, because Celsius has already taken its pain, all of it, and is starting to turn.

Look at the structure. CELH fell from a 52-week high near $66 all the way to $33, cut in half. It then carved a base at $27-28, tested it twice, and held. From that double bottom it has climbed back to $33, about 20% off the low, while my BOTTOM signal has now fired for 11 straight sessions on the name, the strongest persistence read in my screener this week. Rather than pinned at its ceiling like the names I might normally reach for at the highs, it is lifting off its floor. In a tape I am re-engaging with carefully, a name whose sellers are already exhausted is exactly where I want the downside to be small.

The thesis sits in three layers.

First, the business. Celsius is a real consumer brand with energy drinks, shelf space, and distribution, not a multiple-on-vibes story. It is the classic case of a fast grower whose stock got ahead of the fundamentals, then overshot to the downside on the way back. The franchise did not break; the price did. And crucially for this letter, it is a consumer name, not a rate-sensitive one, so no bond-market headwind, which is the risk I keep flagging everywhere else. The honest risk: it is still a sentiment-driven growth name, and a beaten-down stock can stay beaten down longer than you expect.

Second, the bottom. RSI has recovered from oversold to a neutral 55, turning up rather than stretched. The base at $27-28 held on two tests, which is what gives the stop a clean place to live. Volume is heavy enough ($350M+ traded a day) that I can size it without slippage. And there is no earnings report inside the swing window, so no binary event to blow up the setup. This is a structural bottom with an actual turn underneath it, not a falling knife I am trying to catch mid-air.

Third, the asymmetry. If the broadening continues, a destroyed momentum name with a real franchise mean-reverts hard toward the $40s as the shorts cover and the sellers run dry. If the tape wobbles on the yen or the bond market, the downside is already mostly spent. It fell 50% to get here, and the base gives me a defined exit.

🧘 The Philosopher’s Corner

The hardest discipline in this work is not holding a view. It is holding it loosely enough to let the evidence move it. We all know the line about a strong opinion, weakly held. The weak hold is the part almost nobody manages, because a view you have stated out loud starts to feel like a possession you have to defend.

The Stoics had a cleaner way to see it. Marcus Aurelius wrote that if someone can show him he is mistaken, he will change gladly, because what he is after is the truth, and the truth never harmed anyone. What harms you is persisting in your own error. The data this week leaned constructive. My job is not to argue it back into agreeing with the position I have been holding. My job is to update what I do in proportion to what it shows.

See you next week,

Daniel

Disclaimer

This newsletter is for educational and informational purposes only. It is not financial advice.

The content reflects personal opinions shared publicly as a journal. Trading stocks, options, futures, or any financial instrument involves significant risk. You can lose your entire investment. There is no guarantee of profit.

The author is not a registered investment advisor, broker, or financial professional with any regulatory authority including the SEC or CFTC. Always consult a licensed financial advisor before making any investment decisions.

By reading this newsletter, you accept full responsibility for your own trading and investment choices. Past performance does not guarantee future results. Markets are unpredictable.

Screenshots are courtesy of TradingView, VixCentral, and other platforms with which the author has no affiliation. Information shared may contain errors or become outdated quickly.

This content is the intellectual property of the author. Copying or redistributing without permission is prohibited.

By continuing to read, you acknowledge and accept these terms.

Read the desk every week

Market analysis in plain English, plus the app that scans the whole US market for you.

Become a member Read the original on Substack ↗